About sixteen years ago, I met him for the first time. My trainwreck sibling brought home this adorable puppy he had no business adopting because he had not one thing in his life that wasn’t a mess. I was furious at my sibling – he didn’t even take care of himself, how could he drag

Read More

March 26, 2009

I’m steaming over the loss of the entire post that should have gone up yesterday, but didn’t. Instead, I tried to post it from my phone’s web browser, had to edit the title, and somehow lost the entire post!

Oh well. Y’all probably didn’t need the long version anyway. Here’s the summary:

Professional

1. Attended another (wait listed) class for my Certificate program this week. Would have missed this opportunity if I hadn’t called and asked for it; you’re supposed to sit and wait for them to contact you when there are openings but I couldn’t afford to be passive. (Never mind I was late thanks to the take-many-detours shuttle driver. Have I ever mentioned how much I HATE being late?)

2. Requested permission to “crash” another course two weeks ago. We’re down to the wire here, so I absolutely have to hit every class if I want to take my Certificates of Supervision and Management before the layoff. This means my assertiveness is getting a major workout.

Financial

1. +40: check received from the Airborne class action settlement.

2. +10: my first payout from MySurvey.com

3. +226: this is really a refund, not a plus sign. My dad peeved me because he had over 30 days to return the Dish Network equipment but didn’t so they charged my card. Now I have to wait for them to acknowledge and process receipt of the equipment, process a manual return, and then request a manual refund from the credit card. Bleh.

4. +153: Still waiting for the credit card to send a check from the second insurance refund. Meh.

Fun/Consumerism

1. LOVED MoneyFunk’s latest project: a turtle Amigurumi! I’m a total sucker for cute turtles.

2. Have plans for a $22 prix fixe dinner with a friend next week; a treat is usually a $4 cheeseburger or a couple of chicken soft tacos, but occasionally I have a hankerin’. And it’s at a restaurant I can’t ever afford, normally.

March 24, 2009

I loved MoneyDummy‘s crochet project where she magicked old sheets into bathroom rugs. Make that projects, plural. It’s not just because it’s so creative, but also because it transforms something formerly grubby or less than desirable in its original form and gives it new life.

I was about to try to be that ambitious, but realized I probably should wait until I have new sheets to replace the old ones before I had three new bathrugs and zero sheets. Pff, practicality!

Instead, as part of the great closet clean-out that’s dragged on for weeks, months (!) I was giving up old tops that just had a bit of sentimental value or I just couldn’t Goodwill or discard entirely. And the great thing about fussing and cleaning on the telephone with your BFF, other than the moral support and feeling like it was good ole high school days again, is that she often comes up with great ideas. Can’t toss old shirts? Take ’em to her ma!

Why?

Because her ma is a flippin’ crafty genius, and turned it into this handsome devil of a quilt:

That corner’s folded down to show you the lovely no-pill fleece backing. The blue-purple squares that are kind of shiny is a suede (washable!) sort of material, and that almost Hawaiian purple print used to be my scrubs from my animal hospital days. Unfortunately, the flash doesn’t do justice to the redder floral bits.

That corner’s folded down to show you the lovely no-pill fleece backing. The blue-purple squares that are kind of shiny is a suede (washable!) sort of material, and that almost Hawaiian purple print used to be my scrubs from my animal hospital days. Unfortunately, the flash doesn’t do justice to the redder floral bits.

Isn’t that cool? Someday, I will learn to do this for myself. Someday!

March 23, 2009

Can it make Mondays better? Here are a few fondly remembered meals of my once-extravagant business-dinner past:

Oh, formal business dinners, how I miss thee ….

Oh, formal business dinners, how I miss thee ….

Apologies but I can’t identify all the meals by name/restaurant, it feels like that would be revealing too much. (For example, how poor my memory is, for one thing!)

Apologies but I can’t identify all the meals by name/restaurant, it feels like that would be revealing too much. (For example, how poor my memory is, for one thing!)

And I know we had some spectacular salads, too, but I can’t find those pictures, so wee cute little dessert will have to suffice.

And I know we had some spectacular salads, too, but I can’t find those pictures, so wee cute little dessert will have to suffice.

And I can assure you, all those fancy dinners did not make me a food snob. While they were delightfully, sinfully delicious, I truly appreciate my plain food routine after all the rich foods and eating out.

And I can assure you, all those fancy dinners did not make me a food snob. While they were delightfully, sinfully delicious, I truly appreciate my plain food routine after all the rich foods and eating out.

March 20, 2009

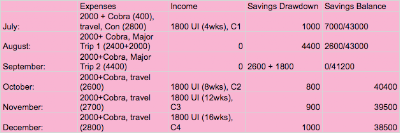

It’s funny how an increment of $10k can evolve a game plan. Now that we’re past anticipation of and well into preparation for the layoff, I’ve been dabbling with numbers and colors on Google Docs spreadsheets. I need to know we’ll be “ok” if this trend of employers passively rejecting me, ie: not calling me back, continues.

Multiple scenario budgets have been projected based on remaining unemployed through December 2009. Barring emergencies, they reveal that:

A) We will be ok until the end of this year.

B) Assuming unemployment will supplement savings, we’ll survive beyond the end of this year.

C) I can afford to take at least one major trip (<$2000). For sanity's sake, I can't afford not to take that trip.

These revelations are fairly reassuring, at least until the New Year, at which point full scale, high grade panic will commence if I don’t have a job nailed down. It doesn’t matter if I still have $30k in cash. Without cash flow, I will be freaking out. Consider yourselves warned.

These three iterations made the most sense for modeling purposes.

Scenario 1: With full expenses, no major travel, unsubsidized Cobra

Scenario 2: With full expenses, two major trips, and unsubsidized Cobra

Scenario 2: With full expenses, two major trips, and unsubsidized Cobra

Scenario 3: With full expenses, two major trips, and subsidized Cobra

Scenario 3: With full expenses, two major trips, and subsidized Cobra

Notes

A) Both vacation and severance payouts are estimates, to be paid at the beginning of July.

B) “Travel” money every month is just an allowance. It’s not much, but you better believe I’m not just sitting on my butt at home all day every day.

Some thoughts. If anything goes wonky with severance and vacation, knock $5000 off that starting savings total. That’s a just-in-case. We’ll likely know by mid-June if they intend to be obstreperous.

I’d like to contribute $5000 to my 2008 and 2009 Roth IRAs, so subtract $10,000 total from the savings balance. But if I end this year with no new job lined up, that leaves between $23,000- 28,000 to start the new year.

Um. No. Voluntarily dipping below $25,000 cash savings is an no fly zone. Going below that number makes me fear for the still-nascent house fund, among other things. $30,000 would be much better. $40,000, even better. But you can see where this might lead: no trips, no rest, no travel, no life, no balance. While I’m fiscally conservative, timidity in financial planning is not my thing.

Speaking of fear, everyone’s fearful now so, according to Buffett, it’s time to be greedy. Not too greedy, but I do want to set aside some non-retirement investing money while the market is still trashed. Buy low, yes? A thousand bucks’ll be plenty because that low, low price might very well turn into zero.

After some consideration, I think this is the plan:

1) don’t allow anything to go awry with severance and vacation. Don’t mess with my money, boss!

2) don’t contribute to my 2009 Roth.

3) do contribute to 2008 Roth. ($-5000)

4) consolidate emergency cash into a single account, probably a money market given the state of my existing “high” yield savings accounts.

5) continue job hunting

6) plan an awesome trip that includes educational facets that I can add to my resume

7) find a few CDs and create a CD ladder for some of that money

8) research stocks, see if I can muster the confidence to commit to a few

If 2010 dawns with new job secured, I can contribute to my 2009 Roth, salt away something for the emergency fund while replenishing the expense cushion, and start seriously funding the house account. Ideally, that new job would require a move of reasonable distance and affordability.

Lists and spreadsheets laying out possible outcomes in a situation largely out of my control helps me focus my attention where it’ll do the most good. Then I can look at this job loss dead in the eye and call it opportunity.

March 18, 2009

It’s an emotional and physical off-roading sort of week, so I’ve been uninspired. That was going to be the thrust of the post, but complaining’s not going to help. (Or hasn’t, yet.)

Thusly, we’re going to practice optimism, today, because:

1) it’s Wednesday!

2) I found a highly challenging job listing that I’m a little underqualified for but I don’t care, I want it anyway. And I could do it, if they would overlook the lack of a Master’s degree. Promise.

3) and Sallie’s Niece got the job!

4) so that means it’s not categorically impossible. [No, that’s not logical. Doesn’t matter.]

I’ve been a bit fed up with my doom and gloom. Luckily, I got it all out over at i pick up pennies (thanks Abby!) Not that I suggest you read my rant, please don’t, just visit Abby if you like.

And 5) Crystal is basking in the sun for me via Twitter, never you mind if she’s playing hooky or not. 🙂

Oh! and 6) I’m actually happy about the layoff now. I’m thrilled to be getting out of here, with severance. You see, I have plans for that money.

Edit for accuracy: We still need our official notice but, as long as I stick it out until June 30th, I should be all good w/regards to severance.

And 7) My doctor’s office (HMO) is ridiculously awesome. I emailed asking for an appt next Tuesday am. Got a VM that the doc was not in clinic that day, was asked to call back. I called to schedule for a different day but had to hang up before getting through. Found a voice message on my cell phone, 30 minutes later, saying that I was booked for the day/time I originally requested. Oh and, “you can come any time you like, your actual appointment is X:00.” They must love me. I want to keep them forever.

March 17, 2009

I’ve been doing some research on all applicable benefits that I need to address, secure or continue after the layoff, most of the information I need is available at my employer’s website. I’ve truncated some of the information for clarity’s sake. It’s very important to make these decisions while I have the luxury of time to think about it because the website explicitly states:

Enroll within the deadlines. If you do not act by the deadlines, you will not be able to purchase the coverage at a later date.

Medical and Dental Plans

Coverage ends on the last day of the month in which you terminate.

* You may elect to continue your coverage for up to 18 months (COBRA). HMO participants who exhaust their initial 18 months of COBRA coverage may be eligible for an additional 18 months under Cal COBRA. Your election must be returned to the Benefits Administration office postmarked within 60 days from your termination date or the date of notification, whichever is later. If you do not elect COBRA within 60 days, the COBRA opportunity is forfeited. You will pay the full premium plus a 2% administrative fee.

~ It’d be ideal for me to schedule my last day in the first week of the month if I have a choice. (Doubt it). If I leave due to securing new employment, I should not *fingers crossed* need to worry about COBRA. I’ll keep the paperwork on hand anyway, just in case.

Something I did NOT know before: according to this New York Times article, I should try to wait until the end of the election period to take COBRA to avoid paying for those two months of coverage if possible. If it turns out I needed coverage in Month 1.5 post layoff, I can just make up the two months’ worth of premiums and still be covered. I will, of course, check with the benefits department to make sure that’s true. And get it in writing. 🙂

Life Insurance

Group coverage ends on the last day of the month in which you terminate. Coverage may be converted without evidence of insurability if you apply within 31 days of termination.

~ If I haven’t selected outside insurance by that date, then I’ll convert. For the time being, I’ll apply for supplemental insurance at 5X my current salary in case I want to take it with me. The life insurance quotes I’m getting aren’t so attractive.

Accidental Death and Dismemberment Insurance

Coverage ends on the last day of the month in which you terminate. Conversion to an individual plan must be made within 31 days of termination.

~ Do I really need this?

Long Term Care

Coverage through payroll deduction ends the last day of the month in which you terminate. You can continue coverage by making a direct payment to the insurance company. Your premium remains the same. Contact the carrier directly within 31 days of termination to convert to direct billing.

~ Continuing negotiations with my dad. Better make it snappy!

Old Retirement Plan

If you have satisfied the vesting requirement and the present actuarial value of your benefit is less than $5,000 when you terminate employment, you will need to take action regarding your benefit. If you do not take action regarding your benefit, we will cash out your money to you if the value is $1,000 or less. If the value is $1,001 to $5,000, we will rollover your money into an IRA. If the value is more than $5,000, you cannot receive payment or rollover the benefit but will receive retirement benefits based on its value when you retire.

~ Vesting was dependent on 5 years of employment so I wasn’t counting on this. It was funded entirely by my employer so I wouldn’t be out of pocket but when I got in touch with the plan supervisor, she told me I was auto-vested when they changed our plan. Nice! I will roll it over directly into my Vanguard account, but she won’t tell me how much it’s worth until I know that my time here is done.

Current Retirement Plan

Your contribution to the Retirement Plan will be taken from your final paycheck. Supplemental Retirement Plan contributions are not taken automatically. Contact your investment company or your benefits office to discuss options regarding your retirement account.

~ Simple, I have enough in the these accounts to maintain my relationship with Vanguard after separation.

Flexible Spending Accounts (FSA)

You may submit claims for eligible dependent care services incurred through the end of the calendar year in which you terminate. You will be reimbursed up to the amount remaining in your account. Expenses submitted for reimbursement must be incurred prior to your termination unless you elect COBRA continuation of your health care FSA on an after-tax basis.

~ Will make sure to be seen by all my doctors, have prescriptions filled, and costs reimbursed before we’re outta here. Doesn’t make sense that I would continue FSA on an after-tax basis since the point is that it’s a pre-tax benefit.

Tuition Assistance

If you leave during a semester, you will receive a pro-rated fee bill and are responsible for paying the cost of tuition for the remainder of the semester.

~ N/A for me. Unfortunately, I never took advantage of this benefit.

Looking back, I’ve been quite blessed to have such comprehensive benefits even if I didn’t fully maximize all of them. Other than the health care, the tuition reimbursement could have paid the largest dividends over time in terms of furthering my career if I could have made time to attend classes. On the other hand, I did manage to earn a major raise by working my butt off instead of taking classes, which was hugely critical to my ability to pay the bills, pay down debt, and save so much. If I can land another job with similar benefits, I will definitely take advantage of free (though taxed) education!

March 15, 2009

After the hike yesterday, my joints are rather sore and I’m in need of some resting up to head off a major ‘ritis flare-up. Therefore, health day!

The shoulder has been out of whack for a long time, so I’m getting that worked on today. We’ll have a late lunch of cheese pizza and salad, and catch up with some old friends.

The Futility Fund (administered by Vanguard) was infused with the Rollover Contribution, finally. That’s $800+ down that drain. 🙂

I’m still waiting for that last insurance reimbursement check from the credit card company, though. Should call and find out what’s taking them s’darned long this time.

Hope everyone else is having a fabulous day!