About sixteen years ago, I met him for the first time. My trainwreck sibling brought home this adorable puppy he had no business adopting because he had not one thing in his life that wasn’t a mess. I was furious at my sibling – he didn’t even take care of himself, how could he drag

Read More

April 27, 2010

My friend asked me if I was going to buy a token something for myself when I got my first paycheck. Suggestions abounded. They sounded awfully nice but nothing really blazed up my desire. Well, a netbook, but that’s no kind of a “little” treat running between $400-500.

It’s just stuff. I just spent two weeks organizing, cleaning, and weeding out stuff with still more of it to do.

Besides that? I have a job. I’m facing down huge challenges and I’m getting paid to do what I wanted to learn how to do. I have the opportunity to make a difference in the lives of at least a few people.

What object is necessary to “symbolize” my intrinsic satisfaction? By its very nature, my “accomplishment” suffices. What need do I have of obtaining an object as a reward for doing a job? [That’s what payday is for!]

I’m not above enjoying goodies like the new clothes that were necessary, and I sure don’t mind having the pocket money to have a meal out once in a while. But a reward simply for having a job? The truth is, I don’t need any rewards for doing my job. A job is a contract wherein I ply my trade and the employee pays me a fair wage for that. I’m ok with that.

April 26, 2010

This is probably the most important detail in the whole process of budget-making: how do I ensure that I have saved a substantial amount by the end of the year, even on an incredibly tight budget?

Step One was establishing my bottom-line expenses. I know that they will increase but for now, I need to know the precise minimum I *must* have.

Step Two was establishing my savings wish list. This is what I want and mean to have. On a meta-level, I know that I have a priority list and can switch priorities as necessary.

*Investing in a 401(k) will be automatic and basically invisible.

Step Three was re-establishing my time commitments. I rely on alternate income to make up the difference between the regular income and the goals and that requires careful time management so that I don’t drop the ball on either side.

Step Four was setting up tracking spreadsheets for the income generated so I stay abreast of the tax implications of freelance work.

Step Five is pulling it all together: as income is earned after the month of April, a set amount will go towards the expense fund and the rest will go to savings. All alternate income goes toward the savings goals as well.

My priorities

Providing for my family

Rebuilding my portfolio of savings and investments

Making time to enjoy my new life

The numbers

Expenses: A very conservative $2,800 per month

Savings: I aim to average $400-500 per month on freelancing = $4950-5850/this year. That takes care of my debt to self which is the same as 50% of my Emergency Fund rebuild goal. I would then take the rest and stash it in the insurance and maintenance funds.

It’s a little disappointing to see the numbers are so low, but any other windfall gigs aren’t included in that total. It’s ok, this is a work in progress.

{———-Bonus Round———}

And we now know that I have to budget in extra money for further medical treatment and therapies for my mom (to be determined) as well as to move them. Look forward to Budgeting, Redux!

April 25, 2010

It’s meant to be my supremely lazy Sunday by which the following are banned from my list of Things To Do: no cooking, cleaning, laundry or other chores.

Instead, SO kindly scribed the following stress-free suggestions for consideration:

– Buy a cardigan for the office; these bones would greatly appreciate extra warmth, p’rhaps a parka?

– Go out for brunch; there are a few folks about the area I coulda shoulda called up

– Massage; medical necessity, actually

– Reconnoiter the local garage sales on Craigslist

– Check out the Martin and Osa sales online

– Use the BOGO coupon at Jamba Juice

It’s a cute idea, but right now my idea of destressing actually includes: not spending money, not leaving the apartment, and catching up on work. Taking out all the housework is splendid though I will pay for it later.

It seems nonsensical, but hear me out. At least one-third of my stress is powered up by the knowledge that I have a million things to do and bills to pay. The balancing act of living frugally and earning “enough” is precarious and altogether draining. As it is, just not pre-cooking for the week would have me in knots if I weren’t at least well ahead of the game on one freelance project after logging hours yesterday evening.

Thanks in no small part to rising early (another abnormality when I’ve got any choice about it), today has been both semi-productive yet restful. There’s a banana nut cake with extra walnuts cooling on the stove, some leftover Indian food warming in the oven, and not an unmanageable amount of work slated for today.

I haven’t watched any TV yet (Serenity! Battlestar Galactica! Dr. Who! White Collar! Bones!) this weekend, but if I wrap up at least another project by mid-afternoon, I could still squeeze in a geekfest. After I defrost the chicken, that is. A girl has got to eat something, sometime this week.

Bonus Question: should I trek out for this week’s coupons and a few bags of Trader Joe’s pretzels for work? I need carbs to get through the day.

April 24, 2010

This is one of the less awesome Saturdays because frankly, this week bit. My homemade chicken soup (above) would really hit the spot. Unfortunately, it didn’t survive past the cook night. It was that good 🙂 It was a very simple soup made with homemade stock, a little salt and pepper and fresh veggies.

It’s been a rough week – I’m dragging after an 8-9 hour day, and by Friday I’m drained to the dregs. I was concerned about getting back into the groove of a working schedule, and thus far my concerns were merited. This is the first weekend I’m deliberately not cooking for a week and cleaning because I have got to get some rest. And I’m taking advantage of the extended Spa Week deal at a local spa – maybe a hot stone massage will alleviate some of this pain. Luckily, the FSA is set up so that should defray the cost.

Family’s got me on the ropes, as usual. Mom was released last night, but Dad’s considering pursuing some alternative treatments which means I need to come up with another $500 a month to pay for it. I don’t mind the cost, it’s just going to be rough getting even more creative.

Some links to love

Frugal Scholar’s had a taste of blog anxiety to go with her broccoli soup; I’m certainly not immune to her feelings: “And, of course, I am somewhat paralyzed by the desire to write a killer post.” I try to make my peace with the fact that readers who actually like me when they happen upon me, not just on a good post day, will be the ones who stay and converse.

April 23, 2010

Another pair of pants are in the mending pile. Because, apparently, I can never start a new job without breaking my pants some way in the first week.

Years ago…..

[First week of work.] Thank goodness for scrubs covering the relevant anatomy, I tore out the seat of my jeans, kneeling.

Next job……

[First week of work.] Tore out the seat of my jeans, picking up a pen. Tied a sweatshirt around my waist. Not too high school or anything.

Same as above job….

[Four year work.] Tore the knee out of my jeans chasing after the puppy. And the seat of my jeans.

This job…..

[Second day of work.] Ripped the hem out of the right pant leg.

I guess it’s an improvement that my tuchus wasn’t threatening to hang out this time, eh? And I can probably repair the hem instead of having to buy a new pair of pants. I think.

April 22, 2010

[This budget was developed before

Sunday and

Monday‘s situations, so of course it’ll have to change to accommodate the new developments. But I worked hard on it, so this series is going up anyway!]

These goals are beyond stretch goals since my disposable income doesn’t actually cover saving an average of $2900/month from the end of July through year-end. That’s fine, I prefer to set high goals and find ways to meet most of them than settle. Some of these are overlapping from the previous post so they’ll look familiar, or they might have been expanded. Until my benefits and paychecks settle out, which they will by the end of May, these goals will remain soft.

Long term Savings Goals

Emergency Fund: Doesn’t need too much work. I’d like to ratchet this up to $40,000 by next year so that I can roll $20,000 into any decent interest-bearing, mid-term CDs.

[Need: $5,400]

Expense Account: It’s less than half its former glory. Let’s take it back up to $10,000.

[Need: $5,000]

ROTH IRA: Haven’t made a contribution in years. Let’s fix that by April 2011.

[Need: $4,000]

Short term Spending Budgets

Taxes: If I earn enough freelance income this year, taking no exemptions throughout the year may not cover my 2010 tax liability. If that starts to look iffy, I will restart this savings account and put away 30% of all freelance invoices.

[TBD]

Auto Maintenance:

Credit card rewards alone won’t be enough to cover this category of expenses. I should have at least $1000/car per year.

[Annual Need: $2,000]

Insurance: Car insurance costs $1200/6 months for two cars. I’ll be canceling my current -very costly- private life insurance because my employer-sponsored version has become active at $9/month and “save” $41/month. Renter’s insurance is another $500/year.

[Annual Need: $2,900; current policies are paid through to October or this time next year]

Travel: Oh for an endless travel fund! Realistically, I should save for the two trips I’ve already committed to (San Diego and going home for a graduation). And maybe two more trips back home this year.

[Need: $2,000; have some travel credit on hand already]

Clothing: I must have a budget for 2011. The budget strings will simply be too tight for me to steal a little bit here and a little there from the Expense fund like I used to do (shhh!).

[Need: TBD]

April 21, 2010

New job, new salary, new savings goals

Ever since landing the job I’ve been on fire to write up a new budget and set my savings goals for the year. With a new set of demands on my income, I had no idea how much I’d be able to save but I’m bound and determined to work it out.

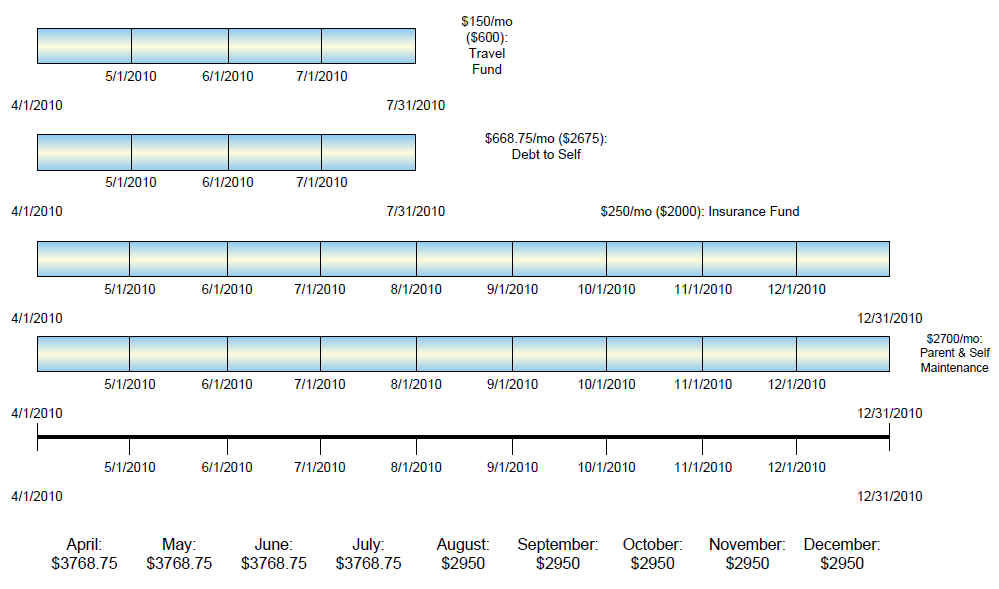

Let’s look at my major obligations

In a nutshell, the graph shows these items:

$2700/mo – allocated for all household expenses (my parents + mine) [SPEND]

$668.75/mo ($2675 total) – Debt to self to be repaid by July [SAVE]

$200/mo ($2000 total) – total amount needed to pay next 6-month auto policy and the monthly savings amount to pay annual insurances. This estimate might be a little on the high side but I need to replenish my insurance fund. [SAVE to SPEND]

$150/mo ($600 total) – travel fund minimum by July [SAVE to SPEND]

Those monthly totals are more than my salary alone can provide, so it’s good to know how much more I need to earn through freelancing. It’s stressful seeing a shortfall, but better to know than not! To be honest, none of that’s actual debt either, what I’m really planning are my short-term savings goals above.

[This budget was developed before

Sunday and

Monday‘s situations, so of course it’ll have to change to accommodate the new developments. But I worked hard on it, so this series is going up anyway!]

{————-CARNIVALS————-}