April 23, 2010

Another pair of pants are in the mending pile. Because, apparently, I can never start a new job without breaking my pants some way in the first week.

Years ago…..

[First week of work.] Thank goodness for scrubs covering the relevant anatomy, I tore out the seat of my jeans, kneeling.

Next job……

[First week of work.] Tore out the seat of my jeans, picking up a pen. Tied a sweatshirt around my waist. Not too high school or anything.

Same as above job….

[Four year work.] Tore the knee out of my jeans chasing after the puppy. And the seat of my jeans.

This job…..

[Second day of work.] Ripped the hem out of the right pant leg.

I guess it’s an improvement that my tuchus wasn’t threatening to hang out this time, eh? And I can probably repair the hem instead of having to buy a new pair of pants. I think.

April 22, 2010

[This budget was developed before

Sunday and

Monday‘s situations, so of course it’ll have to change to accommodate the new developments. But I worked hard on it, so this series is going up anyway!]

These goals are beyond stretch goals since my disposable income doesn’t actually cover saving an average of $2900/month from the end of July through year-end. That’s fine, I prefer to set high goals and find ways to meet most of them than settle. Some of these are overlapping from the previous post so they’ll look familiar, or they might have been expanded. Until my benefits and paychecks settle out, which they will by the end of May, these goals will remain soft.

Long term Savings Goals

Emergency Fund: Doesn’t need too much work. I’d like to ratchet this up to $40,000 by next year so that I can roll $20,000 into any decent interest-bearing, mid-term CDs.

[Need: $5,400]

Expense Account: It’s less than half its former glory. Let’s take it back up to $10,000.

[Need: $5,000]

ROTH IRA: Haven’t made a contribution in years. Let’s fix that by April 2011.

[Need: $4,000]

Short term Spending Budgets

Taxes: If I earn enough freelance income this year, taking no exemptions throughout the year may not cover my 2010 tax liability. If that starts to look iffy, I will restart this savings account and put away 30% of all freelance invoices.

[TBD]

Auto Maintenance:

Credit card rewards alone won’t be enough to cover this category of expenses. I should have at least $1000/car per year.

[Annual Need: $2,000]

Insurance: Car insurance costs $1200/6 months for two cars. I’ll be canceling my current -very costly- private life insurance because my employer-sponsored version has become active at $9/month and “save” $41/month. Renter’s insurance is another $500/year.

[Annual Need: $2,900; current policies are paid through to October or this time next year]

Travel: Oh for an endless travel fund! Realistically, I should save for the two trips I’ve already committed to (San Diego and going home for a graduation). And maybe two more trips back home this year.

[Need: $2,000; have some travel credit on hand already]

Clothing: I must have a budget for 2011. The budget strings will simply be too tight for me to steal a little bit here and a little there from the Expense fund like I used to do (shhh!).

[Need: TBD]

April 21, 2010

New job, new salary, new savings goals

Ever since landing the job I’ve been on fire to write up a new budget and set my savings goals for the year. With a new set of demands on my income, I had no idea how much I’d be able to save but I’m bound and determined to work it out.

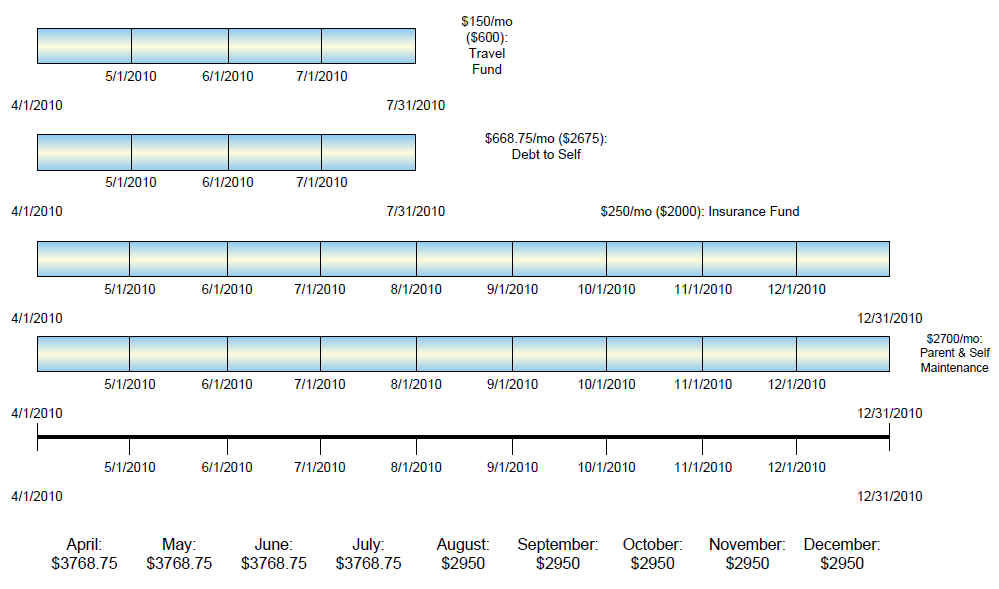

Let’s look at my major obligations

In a nutshell, the graph shows these items:

$2700/mo – allocated for all household expenses (my parents + mine) [SPEND]

$668.75/mo ($2675 total) – Debt to self to be repaid by July [SAVE]

$200/mo ($2000 total) – total amount needed to pay next 6-month auto policy and the monthly savings amount to pay annual insurances. This estimate might be a little on the high side but I need to replenish my insurance fund. [SAVE to SPEND]

$150/mo ($600 total) – travel fund minimum by July [SAVE to SPEND]

Those monthly totals are more than my salary alone can provide, so it’s good to know how much more I need to earn through freelancing. It’s stressful seeing a shortfall, but better to know than not! To be honest, none of that’s actual debt either, what I’m really planning are my short-term savings goals above.

[This budget was developed before

Sunday and

Monday‘s situations, so of course it’ll have to change to accommodate the new developments. But I worked hard on it, so this series is going up anyway!]

{————-CARNIVALS————-}

April 19, 2010

On the heels of one issue comes another: Mom’s in the hospital with pneumonia.

Dad tells me not to worry too much. What’s too much? Because it’s entirely possible I’m already there.

It just seems better.

Days gone by, I liked BART just fine because it does the job but in comparison to Caltrain it’s kind of grubby and a kick in the wallet.

Caltrain’s cheaper for my purposes because they offer a variety of ticket options. Daily or round trips are most costly; the 8-trip and monthly passes bring the daily round trip cost down by 75 cents or $2, respectively. BART has no such options. BART offers a piddling discount off the total price when you buy “high-value” tickets which are just cash-value tickets. The cost of the trips remain the same.

I’ve paid $5 for a one-day round trip ticket, or $17 for an 8-trip pass, that gets me to walking distance of my destination on Caltrain. I would pay $3.25 each way on BART and have to take a bus at both ends for about $2 each trip.

Sadly, while I still haven’t decided about driving into the city for the longer commute in a few months, my only transit option will soon be BART because Caltrain doesn’t go my way.

April 18, 2010

I miss having (the illusion of) a functional family.

My sibling brought home a puppy because he thought he could emotionally manipulate me into letting him keep it when I got back. You know, the sibling with the other dog we have to feed half the time because he can’t afford to. After a few days of romping, the dog gets sick and surprise, she has parvo! I think we know what that means by now.

After two days of sick puppy, he tries to get my dad to call me to help him. And then he calls me himself because my dad won’t do it.

His own dog isn’t vaccinated against parvo! And my dog is old enough that though she’s always been vaccinated, she could be susceptible if it’s truly virulent. There’s no way of knowing. I wanted to reach through the phone and strangle him. He’s an idiot. Now that poor sick puppy has been all over my house shedding parvovirus and he wants me to tell him what to do. And she’s in *really* bad shape.

To recap: he brings home a puppy he is incapable to caring for, like a child, and runs to me to fix it after he’s screwed up.

I just wanted to scream.

I did rip his head off. He and his little friends decided to bring her home, so it’s their responsibility. It broke my heart to say it, but I made it clear that if they can’t (he can’t) afford to take proper care of her knowing that there’s no guarantee she’ll recover, then the only humane thing to do is to put her down because she’s just going to keep getting worse. I think one of them is willing to take financial responsibility whether or not she’s really able to afford it so I hope for the best for the pup.

This won’t be the last time this happens. Obviously the threat of my coming home isn’t enough and I can’t keep dealing with this idiocy cropping up because I’m not there, so I’ve got to start making plans to bring my dog up here with me, and finding a good small place for my parents to live. It’s not going to be easy, it will be expensive, but it has to be done.

April 17, 2010

My first batch of homemade mango salsa, isn’t it pretty? I should have taken a picture of it when I jarred it up in the old salsa jar. That was gorgeous.

I find myself thinking about Versus Matches this morning. As in, “who would win between” or “which is better”? Also about my feels-broken shoulder (it’s not) and how that’s gonna derail some of my super Saturday plans.

Cookery

Extra marinate the BBQ pork [Done!] and cook it this afternoon (+4 hours of marinate time, 1 hr to cook)

Make chicken stock (30 mins prep, 4-6 hours of simmering)

Defrost and bake chicken thighs for next week’s dinners

Prepare ingredients for hot pot dinner (not sure it’s worth the clean-up after, not with this shoulder)

Cleanery

2 loads of laundry

Workery

Freelance gig (3 hours)

Off the cuff writing (1+ hour)

Budgetary

Bekins coughed up a refund check, to be deposited.

UI still owes me a check for the remaining weeks of March, resend claim form. [Done!]

Throwdown Topics, cast your votes (or add your own)!

Roma tomatoes /// Hothouse tomatoes?

100% whole wheat /// Double Fiber bread?

Reavers /// Two By Two, Hands of Blue?

Bank-run Bill Pay /// Account aggregator bill pay /// Service provider Bill Pay?

Headphones /// Ear buds?

Paying less & ironing /// Paying more for no-iron?

Firefox /// Chrome /// Opera?

The mango salsa recipe:

1 ripe mango, diced

2 ripe tomatoes, diced (I use Roma)

1/4 finely diced red onions (use a rougher chop if your onions aren’t lethally spicy)

1/4 diced cucumber

4 cloves garlic, finely diced

Juice of 3 limes; I’m convinced limes aren’t meant to give up their juice

dash of salt

The first batch was handmixed/tossed because I didn’t want to crush everything, but the ingredients are pretty sturdy. Mixing with a spoon is just fine!

It seems to last at least a week in the fridge, I made a second batch and it’s lasting longer and still tastes fresh.