January 27, 2016

January 2015

DROUGHT! DROUGHT! You must use less water because DROUGHT! If you don’t, we’ll be forced to fine you or charge higher rates for higher usage.

September 2015

Good job, you saved so much! The state will now not fine us for being wasteful.

December 2015

Because you used so little water this year, we didn’t collect enough money to cover our costs so we’re charging you 15% more.

January 2016

Use less water! Oh by the way, your bill is 20% higher.

Me: ……

April 28, 2014

I’m moderately techy, but only to the extent that I can get new tech and figure it out with the help of manuals and Google. It’s not something I enjoy or have the spare gray matter to spend on, so my favorite tech solutions have become the ones that are really quick to set up and simple to use. And yet I’m not a huge Apple fan. Go figure.

On one of my last international work trips, it was just easier for me to skip using my phone altogether because it was a bit too old, and my international calling plan options were nearly as terrible as roaming. I just used my iPad to make calls via Google Voice or Skype, depending on who I was contacting, and that worked well enough though I was at the mercy of finding free Wifi to make the connection (I still don’t pay for data for my iPad!)

It felt a bit pre-1990s, scheduling phone calls for specific times when I knew where I’d be and that I’d have a WiFi connection. It was ok since I was working and really didn’t need to call people so much, but still, when you’re used to being connected always, it was a pain to lose the instant communication of texting, IMing, and email.

Last year, I changed out our phones, carriers and plans: spent some big money to get PiC and myself good phones that should last a while (*crossed fingers*) and got us all (including my Dad) on a T-Mobile family plan with a very small company discount and saved some big month on the new plan. We pay $92/month for 2 smartphones and 1 dumbphone: unlimited talk, text, data on the Simple Choice plan. Our data is throttled after a certain amount but it doesn’t matter since it still works ok when throttled. It’s not fun but it’s fine.

Happily for my daydreams of easy international travel and staying connected, I discovered that T-Mobile’s really been hustling – they added another awesome benefit to the Simple Choice plan: free international data and texting!

They offer this in about 120 countries, and you don’t have to activate it, you just have to have a Simple Choice plan and your phone just has to be able to connect to the towers in the country of travel. This is the beauty of competition: T-Mobile’s Simple Choice plan lets you quit them without a termination fee, but they’ve made it so that you’re much less likely to want to!

With international travel (either for business or pleasure) on the calendar for this or next year, it’s relief to have this just built right into the existing plan so I don’t have that moment of panic at the airport, realizing I don’t remember whether I can use my phone without stratospheric charges. And let’s be honest, I want to be able to video call so I can see Doggle, I hate leaving him behind!

September 21, 2011

First impressions rarely survive the heat of examination

“You don’t seem to be the kind of girl/lady who [fill in the blank with any of my hobbies, interests, or responsibilities].”

Talking to @thefitlounge on Twitter about first impressions, I was amused by the idea that anyone could be offended by a wrong first impression. They were pretty standard in my experience whether I meant to give them or not.

In college, I was described as a “Forever-21 seeming kind of girl” as someone’s confessed first impression. As a skinny-@$$ed kid who wore tank tops and jeans on a West Coast college campus teeming with a million other lookalikes, that was not out of line as far as superficial descriptions went. I did buy tank tops at Forever 21. They were cheap, and I had other priorities. (Bills.) That’s not what he meant, of course. He meant: some variety of a spoiled Asian girl with more time and money than brains, at college because her parents made her go not because she had any goals or ambitions beyond pledging a sorority or following the trend of the month, and seeking the most fashion I could find to catch the eye of the hottest guy on campus. We were surrounded by the like, after all.

Since then, I’ve been pegged as all kinds of other similarly superficial, very stereotypical, “female types.” I’ve been pigeonholed professionally by bad bosses as the “bait” for vendors, clients and colleagues (ick, ugh, and laughable), I’ve been initially dismissed as “only a girl” by people who thought I couldn’t possibly deal with the pressure of X, Y, or Z because of my size or my sex, I’ve been blinked at by people who didn’t expect that I’d bleed geek or finance if you cut me.

Growing past the stereotypes

The people who mattered got past the notion, or the outside face if it was an intentional wall I kept up not to let them in at all, that I was not just a 2-D female. They found that I was a person with a brain and the gumption was of my determination, not dictated by size, sex, weight or anything else. They discovered that while I could be just a simple country girl, I’m a little more complex than that.

I’ve lived a bit of life. I’ve flown in a home-built two-seater plane with a oil tycoon to hear the story of how it was built and why it flew better than his other planes; I learned how to ride horses and practiced martial arts; I learned basic car repairs and diagnostics with mechanically savvy friends so that mechanics couldn’t just pull a fast one because gee whillikers, lil lady, this here part that doesn’t exist needs replacing. (Though, shady mechanics will try that with anyone, male or female.)

I’ve adventured to Comic-Con in many phases: as a volunteer, as an attendee, alone, later with friends, and still later, brought friends who had never been. And for the love of money planning, should anyone in real life accidentally ask me a finance-related question, they’ll trigger a flood of information accumulated over the years.

Then there’s all of my background and history that only lives here on my blog – none of my family or financial life is really casual conversation so on meeting me, you might assume that I had a normal family with a normal childhood and had financial support to go to college and maybe held a job or two afterward.

Working with me, you’d be really confused because I still look like some really young age but I hold an incredible amount of responsibility and I’ve got a very strict code of professionalism so I must be old, but … am I? And I’ll never tell how old I am either. Because where’s the fun in that? 😉

The Value of the Superficial Judgment

In all of this, I’d come to realize that while it was valuable that I didn’t actually care what certain people (the average person on the street) thought of me, the fact that in general, people tend to judge based on appearances meant that any efforts put into directing those thoughts could make a difference where it’s important.

I do care whether people think of me as a “young professional” or don’t really think about my age at all because my physical attributes are just groomed enough to walk a middle ground of dressing for success at the level I want to be at but not being casual (like our C-suite) or overly gussied up.

That’s where Shelley’s suggestion of creating a “uniform” of sorts makes sense to me. I can’t afford a fully kitted out wardrobe with a huge variety of options and I don’t need it either. But a small, carefully crafted professional set of clothing to last a week is just about right.

I rely on the first impression that my professional dress will convey: that I’m someone to take seriously because I’m well-groomed and take my job and career seriously, to offset the first impression that I know my usual lackadaisical self would have given. And then my work speaks for me.

In everyday life, I’m a casual person so I dress accordingly so as not to give the impression that I’m anything different. In that “version” of me, I’m not motivated to dress much more nicely on average since I like to be able to play with dogs, read, work on the computer, do household chores, cook, clean, run errands, or any number of random things. And I’m often reserving the good stuff for work. 🙂 I might be cleaning up my act a little bit overall and eliminating some of the far-too-casual from my wardrobe as I creep toward my 30s but on the whole, comfort is the watchword for the weekends.

:: Have you been commonly stereotyped in the past or present? Was it a stereotype that bothered you or worked for you?

:: Are you a different version of yourself in different places?

Related Topics:

Fabulously Broke on Does holding or wearing designer anything, automatically mean you’re a high maintenance shopaholic?

Stacking Pennies on Designer Brands

February 23, 2010

Speaking of yelling “Lifestyle inflation!” at people, I’ve directed that at myself lately, to little avail. I should but cannot imagine going back to a regular phone.

iPhone’s latest antics are: not allowing me to pick up calls, freezing the screen on the call failure screen, refusing to clear it out even after I’ve stopped the call, and shutting down intermittently. Oh, yes, and refusing to accept calls at all, forcing people into voicemail hell, and then maybe informing me of new voicemails an hour or more later.

It’s ridiculous. One major drawback with having an iPhone is that AT&T and Apple get to play the blame game and hang the responsibility for dropped calls on the other guy. In the meantime, stuck in the middle, I feel like a orphan!

On the other hand, some of the functions – which are not limited to the iPhone – such as navigation, internet access, email access (I’m a junkie) are really very helpful in my recently nomadic lifestyle. The navigation is an amazing key to travel independence, and I’m loathe to give it up for a regular phone.

My contract with AT&T is up this month, what shall I do?

Working on the following assumptions:

1. I want another smartphone

2. I don’t want to pay more than I’m paying now ($65/month)

3. I’d prefer not to pay for the phone itself. If I must …. I think the ceiling is at $100. i

4. Trying to avoid as many one-time or recurring luxury fees as possible (activation, for one)

5. My ideal plan includes:

- ~1000 minutes/mo (friends are mainly on two different networks, family on yet a third. They won’t all consolidate to make my life easier!)

- unlimited nights and weekends

- ~300 texts/month

- unlimited email, web browsing and a decent navigation/mapping service

- Even while I have concerns about privacy and security issues, it’d be nice to have the variety of options that the iPhone currently offers for things like banking, stock tickers, and tracking investment apps. It’s not a requirement, though.

This isn’t going to be easy. It may not even be possible. But it’s research time!

Note: In light of my slenderized budget, even $65/month seems like a luxury but do bear in mind this is my connection to the world whether I’m at home or on the road (interviewing, meeting new people with whom I’ll develop professional relationships, being contacted for contract work, etc.)

November 11, 2009

Happily, no jet lag, but definitely a little discombobulation after returning home late. The suitcase remains unpacked which is distinctly odd – opening mail and unloading the suitcase are usually the first things I do when I get home.

Some ramblings for y’all ’til I get it together ….

Audio

Had Ramit on in the background for 45 seconds.

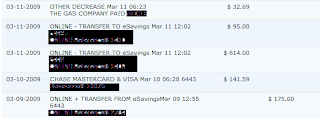

Water Bill

48% decrease. What happened?

Piperlime

These shoes came in, but the day after 7 hours of travel and fat feet is not the time to try on new shoes. I mostly ordered them to check for fit (they have free shipping and free returns), and for the $25 off next purchase coupon.

Returns pile

I went to the trouble of buying a pack of AAA batteries in NY for my mouse. That I left at home in CA. And then found out that I actually just needed a single AA. Back to Walgreens later today.

Cobra/Open Enrollment

This is a whole other post – but turns out I still get to participate in O.E. this November. Oh goody! New rates! Oh wait. …

Netbook lust

I was woefully out of touch this past week because my regular laptop [which I love!] is just too heavy to schlock around the city. The longing for a netbook is pushing me to consider …. dun-dun-duuunnnn…. BLACK FRIDAY!

Feel free to weigh in on that last topic, folks, recommendations, warnings, etc. No enabling necessary! I have set the boundary: it has to be under $200.

October 1, 2009

| Retirement Savings |

Roth IRA: $4,137

401(a):$30,814

Total: $34,951 (33,611)

|

| Emergency Savings |

Catastrophe: $ 35,887

Problem Cushion: $ 1,000

Total: $36,887 (36,963)**

|

| Short Term Goals |

Car Maintenance: $2,244

Insurance: $2,467

Travel/Con: $568

Taxes: $3,590

Moving: $3,994

Total: $12,863 (12,144)

|

| Long Term Goals |

House Down Payment: $102

|

| Investments |

TradeKing: $1,094**

Prosper-ish Loan: $12,630

Personal Loan: $1,500

Savings Bond: $362 (current accrued value)

Total: $15,586 (15,542)

|

| Total Assets |

Illiquid: $34,951

Semi-Liquid: $15,586

Liquid: $36,887

Expense Acct: $7,506

Goals Savings: $12,963

Total: $ 107,893 (105,862)

|

| Debt and Liabilities |

AmEx: $144

Chase: $2,510

Rent: $1,360

Total: $4014 (1,770)

|

| Net Worth |

$103,879 (104,092)

|

A few thoughts …..

Yodlee is all over the place. A few weeks ago, I got an invitation to try their Beta and it kept locking me out of my account. When I gave up on the Beta, the original version kicked me out too! Now it’s showing me bills due two weeks ago that it didn’t think were important until now. Thanks!

Bills-owing are at an all-time high thanks to the school bills (>$1000), and the unexpected traffic fee. That’s eaten into the gains made in the retirement accounts. I’d better hit the books even harder, that quiz I took last night made me sweat!

**Dividend!! My stocks paid out a fat $4 dividend. Marked this one ‘specially because I’m excited. Whoo!

Wonky math. Somewhere in the emergency funds, we’ve got math gone wrong and I can’t figure it out. I never take money out of that account, or at least haven’t yet, but it’s down by a handful of dollars. No time to work on it today, unfortunately.

Changes. This snapshot is useful tracking, but everyone doesn’t need all these details. It’s time to consolidate more accounts and simplify both the system and reporting while preserving the subaccounts I love so much. Currently, my money is spread across ING/ED/Citi/Wamu.

I get free checks from Wamu, Electric Orange can’t serve all my checkwriting needs. Citi is the easier B&M from which to bank with linked checking and “high” interest savings accounts, while the ING/ED accounts have marginally better interest rates. It’s nice to have the flexibility of looking for either Chase OR Citibank branches when I’m travelling rather than hoping for one or the other.

I’m looking for a single bank with B&M and online access, free checkwriting (paper and electronic), ability to manage sub-savings accounts with good interest rates, and no fees. Too much?

August 14, 2009

FB’s post on keeping up with her credit card transactions explains a very similar technique I used when my family was still involved in my finances.

They had credit card debt, half of which had been balance-transferred to my name, they had regular rent/utilities bills which weren’t always covered by their income, they had loans from me, the list ran on for some length.

My finances became this huge non-linear web: income (mine) – outflow (mine) – income (parents) – outflow (theirs) + income (mine) to cover their outflow – outflow (brother’s) + income (mine) to cover his inadequate or non-existent income.

To make things even more complicated, there were debts I’d forgiven, there were new debts accumulated, there was irregular income, irregular overtime, and periods of non-payment. The budgeting calendar was a hot mess!

Eventually, the best way to coordinate things during the time before business credit cards (to divide and track our purchases by user) was to tally each deposit and outgoing check by highlighter and separate transactions.

Every single payment from the family was labeled by name (Dad), amount ($50), reason (loan), and type (cash). While the check ledger was never reconciled in the traditional sense, each outgoing cash loan was recorded, and later struck through once a payment was recorded and

color-coded.

Nowadays, payments are only bundled when I’m scheduling them for bills to be paid out within the same week, preferably in the same day.

As long as a quick glance shows that each transaction is accounted for, I don’t have to worry about running short on funds, overdrawing, or any such thing. Saves me time and fuss, it’s my form of automation.

Ms. Ginger touched on this yesterday in her combo confessional and fix-it post. She and I must be channeling each other this week. 😉