April 21, 2010

New job, new salary, new savings goals

Ever since landing the job I’ve been on fire to write up a new budget and set my savings goals for the year. With a new set of demands on my income, I had no idea how much I’d be able to save but I’m bound and determined to work it out.

Let’s look at my major obligations

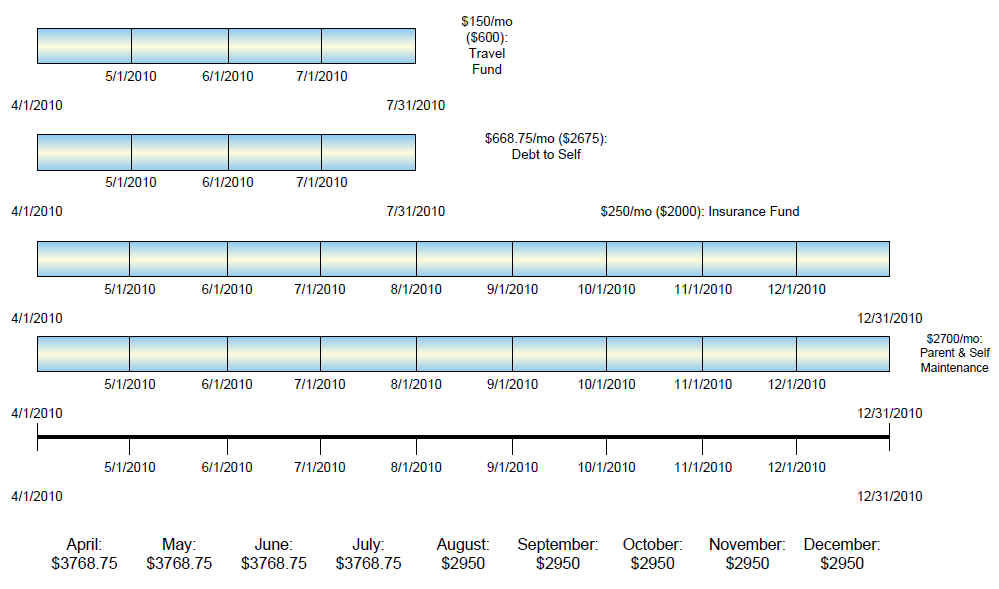

In a nutshell, the graph shows these items:

$2700/mo – allocated for all household expenses (my parents + mine) [SPEND]

$668.75/mo ($2675 total) – Debt to self to be repaid by July [SAVE]

$200/mo ($2000 total) – total amount needed to pay next 6-month auto policy and the monthly savings amount to pay annual insurances. This estimate might be a little on the high side but I need to replenish my insurance fund. [SAVE to SPEND]

$150/mo ($600 total) – travel fund minimum by July [SAVE to SPEND]

Those monthly totals are more than my salary alone can provide, so it’s good to know how much more I need to earn through freelancing. It’s stressful seeing a shortfall, but better to know than not! To be honest, none of that’s actual debt either, what I’m really planning are my short-term savings goals above.

[This budget was developed before

Sunday and

Monday‘s situations, so of course it’ll have to change to accommodate the new developments. But I worked hard on it, so this series is going up anyway!]

{————-CARNIVALS————-}

April 14, 2010

Oh, the excitement of having benefits again!! I’m already a forms + applications geek, but it’s been 9 long months since I had the privilege of drawing a paycheck from whence benefits sprang.

Health

There are about 15 different plans administered by 4 different health care providers. I took the path of least resistance and re-upped with Kaiser for now because I’ve heard good things (via Carrie Actually) and it was the cheapest premium with the most coverage. I’ve never had a problem staying in-network and I hope the healthcare providers in this area are good enough that trend continues.

Dental

I’ll go with the ubiquitous provider here, and this coverage is 100%. I’ll only have a minimal deductible, and the usual $1500 annual benefits max.

Vision

Surprisingly, they’ve got vision covered. I haven’t had a chance to evaluate the plan closely but my vision needs tend to be simple. Thanks to a long-term treatment, I have to have an eye exam every year which I should get anyway. Also, covered 100%.

Life Insurance

The usual 2x salary benefit is covered, and I opted for an additional $200k which will cost me $9/month. I can now cancel my outside coverage that costs quite a bit more per month ($50).

Short term/Long Term Disability

Covered 100%.

Flexible Spending Account

I opted in. Of course!

Commuter Benefits

Also opting in though I’ve never used it before. You can use it for both parking and transit. Even though I have the car, I’m going to take public transit when I can. Wageworks is sassing me, though, so it’ll probably take until next month to become effective.

My monthly cost should be around $250 – mostly pretax. A pretty amazing deal, considering the economy.

March 30, 2010

My experience with Peninsula life, and canvassing people who live in the specific area that I’ve moved to, all said: get your own car. While I could have borrowed a car for most simple runs, that car is a manual transmission and I’m not comfortable enough in it yet to drive without a whole lot of adrenaline-nervosity. (I don’t know about y’all, but the fear of hurting someone else‘s car is nerve-wracking.)

On bad joint days, I would never be able to handle a manual. They don’t happen as frequently as before but when they do, I’m out of commission.

Stacked with the managerial duties that will call for unpredictable early mornings and late nights, I don’t fancy relying exclusively on the three-five transfer public transportation option. There will be times that it works out, but not always.

Don’t get me wrong: I love the lower overall costs of commuting via public transportation and did it for nearly five years in a region that isn’t known for good pub trans. But after creating a whole spreadsheet comparison, I’d either have to add 20-30 minutes of bus time ($) or drive half the round-trip commuting distance just to get to a transit station and add the cost of parking ($$). All told, I’d be spending just as much on transit as my driving commute would cost, and would not be reducing my driving footprint (that’s a terrible mix of terminologies).

Outside of the work commute, there are very few things that are within walking distance (less than 2 miles) and even when it is, the skies have been known to open up unexpectedly halfway through. And the wind blows the rain sideways. I’m a SoCal girl! I’m intrepid but you understand that I don’t have the luxury of changing multiple times a day to stay dry. We have to be a bit more life-practical than that.

As for the money…..

The car purchase will cost me $6800 out of pocket and another $900 for registration and sales tax. The insurance costs $550 per 6 months.

The total cash cost: $8250.

After using the tax money I’d saved and the tax refund ($5575), I owe my emergency fund $2675 and must add $550 every 6 months to my insurance fund.

It’s not the most frugal auto choice I could have made but it was a 6-year-old car in as close to mint condition as I’ve ever seen. That kind of quality is very hard to find in a used car in my designated age range.

I have a plan in place to recoup my Debt to Self through freelance work. If all goes well, I plan to do so in four months.

March 25, 2010

I’ve had excellent dental care over the years courtesy of employer-sponsored benefits, and then thanks to COBRA, so my dental woes have been routinely resolved. My parents, however, have had some dental issues I wasn’t aware of until recently, and I feel guilty about not providing more thoroughly for them since I discovered all was not fine and dandy in their world of teeth. It’s nothing emergent, but I think my dad may need some fairly major work done and I wanted to budget for that ASAP.

My first thought was to get them insured. Naturally, right? It turns out that dental insurance isn’t such a great deal.

A quick review of ehealthinsurance.com showed that I might just be better off self-insuring them.

At an annual cost of $444 plus a yearly deductible of $25 for the cheaper of the only two plans available for this zip code, the policy yields a princely benefit of $500 per person. That’s not all! They’ll offer a grand coinsurance of 0-50% so at times that $500 won’t even be participating in payment of the bills. When it does, it covers no more than 50% of the bill. Essentially I’m paying for the privilege of a partial, sometimes, discount.

The math is only marginally better for the “Enhanced” Plan carrying an annual bill of $1032 with a $150 family deductible. Same lousy excuse for a “coinsurance” and I find myself utterly disgusted. I’d probably be better off saving the cash and sending them to my old (current) dentist with a request for a cash and senior discount.

There’s also a reputable School of Dentistry within 50 miles. An old friend may be able to fill me in on their services or direct me to someone in the know. It’s not a convenient drive, but I’ve heard that they do good work so perhaps on one of the days that he’s free of mom, my dad could get his teeth examined. Their online quote ranges from $50-$88 for an initial exam, all necessary x-rays, study models and a treatment plan. That’s a heck of a lot better than my dentist’s quote of $60 for an exam and additional $35 per x-ray (usually about 4-6 films taken) for a total of $250 for them to tell us what they’re going to do and how much that’ll cost.

Lastly, I should check with my dentist friend about a personal referral. He’s got relatives in the field, they might be more affordable than the local dentist and worth adding to the list of errands they run out in that area.

March 19, 2010

Michelle lit a fire under my butt with the suggestion to get my renters insurance in order. I hadn’t committed to a policy since talking about it in October for a very stupid reason: I was grumpy that my quotes were so high in comparison to everyone else’s. That’s just nonsense. I’m insuring a 3-bedroom house with two dogs and earthquake insurance in California; clearly I forgot I wasn’t comparing apples to apples.

But I’ve finally just bitten the bullet – I’ll be gone soon and won’t be here to take care of anything in case of theft, break-ins, etc.

With the following sage advice from my previous post

@Funny About Money: Be sure it covers full replacement value…that is, what it would cost to buy new stuff. Unless a policy specifically says that (and check with the agent to be sure what the wording means), the insurer may pay you only what it decides is the used value. And used furniture and clothing isn’t worth much, by anyone’s reckoning.

— My policy covers full replacement value.

@The Lost Goat: Make sure the plan covers your comic books … I have to get riders to cover my firearms, because they are not considered general household items. Expensive collectible things like firearms, jewelry, and stamps generally require riders (read: more money) if they are valued past a certain amount.

— A comic book rider will cost something like $15/$500 increment, well worth it. The interesting detail about the rider is that if a loss occurs just to the books, I don’t have to pay a deductible. They would simply pay out the claim in the amount insured.

I set up two policies

I’ve increased my required monthly contribution amounts to the Insurance Fund accordingly to make sure that I’m covered this time next year when the renewals come up. When I get the chance – honestly, probably in a month or so, I’ll rate-review again just in case another company had better rates. I don’t get a multi-policy discount anyway so there’s no real reason to be loyal to a single company if I can find comparable value and better rates elsewhere.

March 17, 2010

I was catching up on my Consumerism Commentary when something Flexo said held my attention: “I believe there are several stages to becoming financially secure or independent. There may be a time where it makes sense to save every cent possible…… I had to survive without a car (relying on friends and public transportation), eliminate cable television, and share an apartment with three roommates. Now that I’m earning more than what I need for basic expenses and long-term saving and investing, I don’t have to be as tight. I willingly give up some income in order to buy myself more convenience.”

Earlier this evening, while discussing the car hunt and the various finds under inspection, a friend asked me, “Do you really need a car? Public transportation won’t cut it?”

My initial answer was a glib “no, public transportation doesn’t quite cut it.” Reading Flexo’s comment above pulled me up short, though. Is that true? Do I really need a car to supplement public transportation or am I taking the easy way out and spending more money I can’t actually afford for convenience? *note: Flexo can afford to expand his spending horizons. I don’t mean to imply that he’s taking the easy way out.*

Since the search began, the budget grew to more than I’d wanted to spend because my requirements haven’t been met. If I’m spending enough to dip into the emergency fund, job or no, the decision has to be sound so I returned to the drawing board to rehash my reasons and evaluate their premises.

Reasons I thought I needed a car

1. Because of the Big Lie and the need to transport my personal effects, I needed a long-term car. A one-way rental is too expensive, a round-trip rental is a waste of time and I’d need to fly back.

— Since relocation was successfully negotiated, I should be able to afford to ship personal effects and fly.

Evaluation: Don’t need a car.

2. Driving would be easier due to potentially abnormal working hours.

— I haven’t experienced rush hour in the metro areas yet so I can’t speak to that, but parking costs between free (minimal street parking) to $20/day depending on the various lots. On average, $7/day, $140/month.

Meanwhile, commuting options exist, though inconvenient. The morning commute would require some combination of two buses and 1 rail system with a minimal amount of walking on both ends ($6.50 – 9.30/day) and travel time of 30 minutes. If the location changes as promised, the new commute requires some combination of two buses and 2-3 rail systems with a minimal amount of walking on both ends ($7-9.30/day) and a travel time of 1.5 hours.

Evaluation: The cost could actually be equal, given the trade-off between commute time/transfers and the wear and tear on the vehicle.

3. I’m choosing to find housing in more suburban areas for more affordability which also lends itself to free parking/no zoned parking.

— If I chose to live in the more urban area, I’d likely be in walking or biking distance of most nearby businesses such as restaurants or groceries, entertainment and shopping. But not #4.

Evaluation: I need more data.

4. My preferences for entertainment are far-flung and while potentially cheap or free, require that I be able to reach them somehow.

— I could always hole up in the room with a stack of books and become a hermit. I’m kind of kidding. The reality is that my preference for entertainment is rarely to go out. I prefer to spend quality time with friends or animals. While that can be low-key, it can only happen if you’re mobile.

Evaluation: At first I thought: I spent several years being a hermit in the name of saving money and paying down debt. But my social network won’t be strong enough to rely on friends for transportation.

5. I need to be independently mobile.

— I need to keep costs to a minimum.

Evaluation: No car.

That last part is really a tosser, though, because I have to be honest – I rated the anti #5 argument higher because I’m afraid to stop being being hardcore, down to the bone, slasher frugal. I’ve lived that way for years. Now that I have two (or 1.5 households) to pay for my instincts scream at me to stay that way.

Meanwhile, a competing sense of self(ishness) says that I’m old enough to be on my own and do what I want, and what I want is to be independently mobile. Is my desire to Stop Sharing so strong that I’d pay the cost of another car?

Let’s face it, a car will cost a lot of money for someone who won’t be making serious bucks.

First, there’s the fixed cost of purchase. Let’s say I go wild and plunk down $10k. A little more than half of that was my tax refund and money saved for two years just in case I had to pay taxes. So a little less than that comes out of the emergency fund.

Then we tack on a conservative $1000 for insurance annually. We also have the costs of maintenance and repairs which are typically budgeted around $1500/year. Remember now, that’s not just for the new car, that’s also for my old car which I remain responsible for. So the insurance and maintenance budget has doubled. Then of course, we have fuel, and since I live in CA we have fuel + $$. Conservatively we’ll call it $100/month, with say, $70/mo for parking assuming I cannot always get parking for free.

Can I afford an annual Convenience Fee of $4540, while replenishing a $5000 hole in the emergency fund?

Probably.

Can I afford an additional expenditure of $4540/year without creating major drag on my savings goals for the year?

Well, unemployment already did a number on them so I honestly haven’t set any, but probably not.

To be fair, let’s compare the cost of public transportation commuting against that annual fee.

On the low end, 20 days a month, 12 months a year at $7/day: $1680 x 2 trips a day = $3360

On the high end, 20 days a month, 12 months a year at $9.30/day: $2232 x 2 trips a day = $4464

I’ll be honest, I didn’t see the math playing out this way. I was pretty sure it’d come very firmly down on the side of public transportation. Tolls (for driving) and fare increases (for commuting) were not factored in as they’re not predictable. In truth, even with the car, I’d likely be doing some pub transportation once I figured out that traffic and parking vagaries so these numbers (and the difference in cost) remain soft. With any luck that would bring the daily amount down on average by half.

At the end of the day, after running the numbers, it’s partly a math and partly an emotional decision. If I’m willing to take the initial $5k+ hit to my net worth on the math side, then my emotional side argues for the buy as well.

I am, in essence, the personification of Newton’s Law. When “at rest,” I tend to stay “at rest.” When I’m limited to sharing a vehicle on someone else’s schedule, I have been categorically a shut-in working on my projects indoors from dusk to dawn and back again, without a break. I leave on the spur of the moment and if that’s not possible then I just don’t bother.

Historically then, my sense of stability and productivity is found in part in my ability to go about my business at will, without wondering if the car’s been taken by the shared individual, without having to cut short my errands or reschedule to accommodate someone else’s schedule. It is, I’ll admit, kind of ridiculous. But that’s how I function and that’s what I have to work around. And it’s kind of more ridiculous to refuse to make a purchase that is mathematically acceptable simply because I don’t want to backslide on my monthly numbers.

Note: the calculations for the car are based purely on the commute numbers, but clearly the car will be handy for longer road trips that are tentatively planned for later in the year. Increased usage would increase cost but it’s the function of the car to be used.

March 8, 2010

No, I’m not getting ready for any major life change personally. It’s just that I’m failing to stay abreast of the tsunami of friends, friends of friends, and family friends getting pregnant and inviting me to every single baby shower, ever. Similar to the previous decade’s “We’re engaged (and we want you in the wedding)!” the watchphrase of the 2010s bodes well to be “We’re expecting!”

Then, inevitably, the baby shower. Most of them are thrown together clutches of women from separate circles of the mom-to-be’s life who are mostly there to compare gifts. I hate the cutesy games that always include a huge diaper pin or the ones where uttering the word “baby” is greeted with hoots and tallied throughout the afternoon. And the cooing. The cooing. I hate baby showers. I know, I’m a monster.

I love babies, I love showers, I even like baby clothes, and I’m very happy for the expecting. But let’s face it, your run of the mill baby shower is just awful.

And when you consider the outrageous cost of all things New Baby people register for, everyone else’s life events can easily run roughshod over your unsuspecting budget. You understand I love gift-giving, but I love good gift-giving. Lacking the yarn wrangling skills (which aren’t cheap) of Mapgirl and Mrs. Micah, I trend towards more practical gifts like clothing in a variety of sizes, plenty of bibs, feeding-related equipment, lotions and potions galore. You simply cannot compile a good baby gift using conventional methods and get out the door for under $100-200. And you know I’m not a get out the door gifter.

If we were only doing this dance once a year, I’d shut up and go along with it, but my cohort numbers at least 20 individuals, and I’m very very close with at least half of them which means I’m on the guest list for their friends and family. This decade, inclusivity will cost more than I can bear unless I “Adapt, Overcome and Improvise!” [Points to whoever recognizes which Eastwood movie that’s from.]

So how do I graciously deal? The same way I dealt with bridesmaiding: be creative and plan far in advance.

Stage 1: Baby clothes can cost more than my personal annual clothing budget, so I’ve signed up for Gymboree’s rewards program wherein I’m showered with coupons and sales notices. Twice a year, they have their Semi-Annual sale where clothes are marked down 50-70%, and combined with coupons and outlet stores, I’ll stock up on clothing for both genders.

Stage 2: Baby-related stuff, being unlimited to any season, doesn’t go on sale the way Christmas, Valentine’s Day or other annual holiday stuff does. So wrapping paper, bags, and tissue paper will be purchased in neutrals and well in advance of any shower invitation. Baskets are a great wrapping aid, and are usually most affordable when found at resale shops like Big Lots, Tuesday Morning or Ross and Marshalls.

Stage 3: My closest friends know that I’m at least financially nerdy, so I’m issuing a declaration that all gifts post-baby shower will be something toward their education. And then I’m either contributing towards the school fund or giving a modest cash gift.

Note: I buy clothing in mostly larger sizes the kids can grow into since most gifts are onesies for 6 months and under. I target 18 months and older and try to find them for $5 or less.