July 26, 2010

I was going to answer all the comments on this post, but my response is long enough to be a post of its own.

I’m not jumping into any fires. I might have moved in but I haven’t completely lost my mind. We’re not sharing money at this point, but we’re sharing some expenses and combining our money philosophies to create something we can both be happy with.

Most importantly – you wouldn’t realize this because you don’t know him so it’s only fair to point it out – he wouldn’t ask me to take on any more, and especially not his mortgage in truth.

He was joking about that and I understood that. I only parsed out what I could shoulder to illustrate how he needs to be prepared if he were to quit his job. And he may well be, but he wouldn’t foolishly up and walk out either.

CaitlinO pointed out that if I’m not splitting all the bills down the middle, he’s subsidizing my lifestyle/savings/family responsibilities. True. And I’m not thrilled with that but the truth is, what I bring to the table is a lot of financial knowledge and a willingness to dig in to any financial situation and improve it. He points out time and again that what I bring to the table is every bit as valuable as the mortgage he pays because I’ll take care of our long term financial health.

I love that my blog friends are so smart, y’all see some part of the truth of what I was sharing:

Frugal Zeitgeist is absolutely right: “the best thing you could possibly do for both of you is be his work cheerleader and number one fan while working together to figure out a backup plan that doesn’t involve bankrupting you. With your good sense as a guide, it sounds like between the two of you, you’ll find a way.”

That’s exactly what I was doing. Using myself as an example, I was sharing with him the economic breakdown of what we’d need to be able to do in a dire situation.

SingleMa understood exactly the spirit of my comment: “It wasn’t a commitment I chose to take on but our relationship is and this is part of the game.”

That made me smile. 🙂 I hope everything works out with your SO’s situation.

Thank you, SingleMa, for seeing the spirit of my post.

Sense made me laugh: also, does he have an e-fund of his own to fall back on? that might make the situation easier to handle, knowing that you’re combining your Forces. You know, ‘Power of The E-Funds Unite!’ and you could get shiny rings and place them together whenever you needed to draw on your new improved dual powers. 🙂

I love this. We totally need Power Fund Rings. He doesn’t have what I consider a good e-fund for his obligations but this situation has enlightened him more to the need. Slowly but surely, I’m turning a spender into less of a spender?

Crystal pointed out the very thing I don’t want to face, what could happen if I didn’t share with him my accountanty brain: Life works out most of the time, but I hope PiC doesn’t quit until he finds something better. Toxic sucks, but so will the fights that start when you start feeling used…or at least, that’s what happened to us.

Funny About Money: If he’s that unhappy with the job, I hope he’s looking elsewhere. It’s a lot easier to get a job when you’ve got a job.

If he’s not at risk of being fired, it might be good for him to consider what my tax lawyer once said when I wanted nothing more than to get away from the Great Desert University: “A sh*tty job is better than no job.”

Not at risk, no, but there’s absolutely every reason for him to find a better place before he becomes so unhappy there IS a risk.

July 19, 2010

“Can you pay the mortgage for a while?”

If you hear that high-pitched squealing, it’s either my tires peeling out of the garage, or the whistle of my brain on overdrive.

PiC wasn’t totally serious when he asked, it was really just out of frustration. He’s been going through a rough patch at the job and it’s at a point where I think it’s toxic. Having been there, I know from toxic and I know it’s insidious. You develop defense mechanisms that are hard to break and stop trusting people. He needs a major change or at the very least, the comfort of knowing that if he wanted or needed to jump ship, he’s financially able to. You know, the e-fund!

As much as I practice financial responsibility here, I don’t preach it everywhere and especially not to someone who is meant to be a partner. We have our differences and discuss them rationally to find a compromise. That said, of course there’s a corner of my brain that goes “poof” like a small atomic bomb. “Why?!?!” it screeches.

Not “why would you lean on me?” and not “why would you even think about quitting?” I know the answers to those questions and I’m fine with it. It’s a very simple “why did you wait until nooowwww to think about this??”

Ok. That’s my vent. Onward we go.

I did a quick verbal calculation for him: worst case scenario, I could support the both of us, and my family, for about 9 months using the cash I have on hand. That would completely drain my cash holdings without accounting for the incoming paychecks. (That is not, as we all know from the unemployment rolls, a very long time.)

At some point in the near future, very near, we’ll have to discuss a more realistic plan than burning bridges or stewing in a bad work environment for the sake of a paycheck, chained down by a mortgage. It wasn’t a commitment I chose to take on but our relationship is and this is part of the game.

If there’s a bright side to this situation, we’ll be talking much more frankly and proactively about money than ever before. And that’s a good thing in my book.

Click here to see the follow-up post, comments and further explanation.

February 3, 2009

The truck sold. What’s next?

Well, I’m pretty sure that the sale price didn’t come close to breaking even against the amount of money I’ve expended on the truck payments since last July, I’m not even checking, but it did cover the lump pay-off sum of $2356, with some cash to spare.

The question is: what do I do with that “extra” money?

My first reaction was to kick that money over to pay off the family car. It’s just about the right amount to pay it off, and would remove one more loan from the family resources. (That car is currently my parents’ responsibility, and not under my name.) It would free up cash flow about 7 months earlier than expected.

My second reaction was to put it in the emergency fund because I’m neurotically squirreling money away.

My third reaction was to leave it in the expenses fund because that’s where the money came from in the first place, and I’m a BIG fan of paying myself back.

Lastly, there’s a hybrid option. I could give them some partial assistance monthly, depending on how much they need to break even between my mom’s (piddling) disability money and my dad’s erratic income. By my calculations, it appears that they should only be running short a hundred or so each month until April. At that time, another monthly obligation falls off the balance sheet, and they should be fine with regards to the few debts I don’t pay for them.

As much as my gut reaction is just to pay it all off, I don’t want to nip this budding sense of responsibility that my dad’s developing. I want to encourage him to work with me because I’m just not up for ANY more shenanigans.

Thoughts?

November 11, 2008

My online “high interest” savings accounts are anything but by now, and it’s past time to do something about it.

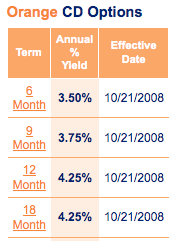

The odd thing is that I remembered seeing a 4.0% APY offer at Citi a couple days ago, and it’s still there when you use the navigational rate selector to check rates based on term length, or amount deposited. In other places, though, like the advert box or when you actually click through to apply, it’s 3.5% APY. What gives?

I should roll over some of my emergency money (it’s spread across three different accounts because I didn’t want to be stuck without any e-money if one of the banks were to encounter problems) in the Citi and ING Direct accounts to CDs since they’re short term and I don’t anticipate needing all of that money upfront. (Oh great, way to tempt fate, self!) Looks like both of them offer a 6-month 3.5% APY right now, so I don’t even have to feel torn between one or the other product.

Then again, I could create a CD ladder with ING:

The only question is, is that really feasible considering CDs are just a bit less than liquid vehicles? I’m crap at math sometimes, bear with me. If my e-fund is at 6 months’ worth of expenses, and I don’t need to touch it for another two months (approximately), I would be safe putting up to 2 months’ worth in a 6-month CD. If I were to need access to the money starting in two months, I would need four months’ of cash (12,000) before the remaining money (8,000) was available at maturation.

That puts paid to the idea of creating a ladder with this money for now. Oh well, just a thought.

October 3, 2008

The long-awaited quarterly check has arrived and I am positively stoked.

I am so close to having six months of living expenses in the Emergency Fund!! As soon as I have at least $1000 in the mini E-fund, my plan is to [finally] close the real E-fund to all non-critical withdrawals.

All the bills for September have been paid and I still have $1300 in the Expenses fund. With the deposit from the quarterly, I have enough for October’s expenses on October 2nd. All paychecks earned in October will continue to add an allotted amount to the Exp. Fund, but I won’t be waiting on them to pay the bills. Holy cow, I could pay the entire month’s bills on October 1st. I won’t, of course, that’s not the point of the cushion. The point is that I could if I needed to. Whew!

So I discovered a few things wrong with my math. The quarterly is for the past three months of work [July 1st-Sept 30th], so plotting the total expenses against income through the end of December means I come up short, ie: depleting most of the expense fund by year’s end.

What I need to do is fund the supplemental portion ahead of the next three months. In other words, instead of taking July-Sept money, and only setting aside three months’ worth of income to make up shortfalls from July-Sept, I should set aside enough for July through December. Then, I’ll be covered and still have the cushion in place through the end of December. Then the last quarterly check of the year [Sept through Dec] funds the various accounts that I’d previously planned for this check: Savings, Insurance, Car Maintenance, Travel, Moving, etc. That means I’ll be funding it for 2009, at the end of 2008! This makes much more sense.

All OT can now go towards other sub-expense funds instead of just savings and expenses. I expect an insurance bill in November and I don’t quite have enough for that yet, so OT will fund savings and insurance for the next month and a half.

Also, I’d goofed on the October paychecks, so I have to rewrite the plans for 4 paychecks in the next two months, not three. And actually, now that I’ve fixed the above problem, that third paycheck can come at any time, it’s no big deal.

It’s very strange budgeting on a hybrid [half regular-half supplementary] income. The supplemental is scheduled and the amount is set, so it shouldn’t be difficult, but I haven’t done it so very well since this started. Might I now be starting to get the hang of it?

Perhaps I’ll even get my September snapshot in order now that I’ve reconfigured the economic landscape …

August 4, 2008

I’m heading out to Portland for a long weekend starting on Friday. My cousin and I are making this a girls’ weekend (aka: no family visits) but since I’m normally only up there to visit family, I have no idea what else Portland has to offer.

We’re going to go hiking, and I’d like to visit Powell’s City of Books since I’ve never been. I don’t want to buy anything, I just want to wander around the books and ogle them.

I’m not looking for touristy things, necessarily, just fun, frugal things to do or see. Does anyone have suggestions?

June 24, 2008

Yikes, it’s already nearly the end of June! Two weeks ago, I realized that June had well and truly started, and if I was going to visit Portland and Phoenix this summer, I’d better get my tuckus in gear!

I missed my chance to make the Portland trip this month, and the Phoenix trip in August, so I thought to cram them both into August. Then I was informed that I was attending a wedding in August with BF. Hmm….. August will be insane if I go on a trip every weekend. Yes, the opposite of relaxing. Also, there’s a sporting event to be attended in October, also for BF. Portland will have to happen in August, Phoenix will probably get pushed to September, I believe. Work is claiming one of my weekends in August, so there’s just more than enough going on that month.

So there’s a lot of travel juggling going on. My travel budget this year is a wee one, so I have to be very creative in mixing award flights, gift cards, and real cash money.

The wedding flight ran $149, just within the $150 budget I’d allowed. I wanted to buy it immediately, and use the $100 GC for the October flight. But I didn’t take my own advice because I wanted to consult with BF about dates and times before I purchased the tickets. He’s still out of town, but I just guessed and purchased the tickets before they went up more than the $15 they already had. *tsk* Yeah, the price went up. No, I’m never going to learn.

I might as well get that SW gift card now so I have the GC and discount code ready at hand when I have to purchase the October flight.

There’s a quiet voice inside me whisper-screaming: Hey!! Skip one of those trips and use the money to pay bills! BILLS!!!

I’m ignoring that voice. I’m ignoring it.

The temptation to skip it all and leave the money in the travel fund “just in case” is overwhelming, but I just don’t see how I can renege after promising over and over that I’d visit these friends for the last few years. The PF blogger in me keeps saying that I’m going to use up ALL of my travel money by October and then what’ll I do? Things at work are still chaotic and I’ve got no plans for replenishing this fund. But that’s what the e-fund is for, Chicken Little. The sky’s not going to fall down if I go and have a nice weekend with childhood friends, and it very well might if I go back on my word!

Terrorism isn’t the reason I’m going, though. If I don’t do it this year, I might never. If I talk myself out of a promise this year, I very well may do so again next year. There’s never going to be a perfect time, at least not for the next ten years because I imagine the perfect time is something like, I have 5 months’s worth of vacation time, $100,000 in the bank for nothing but pleasure, etc. Not. Going. To. Happen.

As it is? I have nearly 180 hours of vacation time. I could be out on sick and then vacation leave for two months.

I’m going to play, dangit.