April 27, 2009

’tis back to the grindstone, m’hearties!

Glad to be bringing home a paycheck for another few (9) weeks, but not so much to have to actually do it. Here. With these people. You understand.

Had a wonderfully *waiting* weekend with the BFF et al. We’re anxiously awaiting her new bundle of joy and have bets going on how much he’ll weigh. Your positive thoughts are much appreciated, I’m worried that he’s been so quiet.

We had other good news to celebrate: her sibling is engaged and will likely be having an Aussie wedding. I promptly texted my congratulations and asked if I was invited to the shindig. 🙂 [Yes, I am.]

I figured that I should invite myself early on to guarantee that I can find a decent flight. I’ll be doing my travel research soon, it’d be so cool if I were, ah, still unemployed and able to do a NZ and Australia jaunt in the fall. [Cool minus the part where I’d still be jobless ….. priorities, priorities…!!]

Oh, and I just realized that this will be the first wedding that I’ve attended in years where I won’t be part of the ceremony. Oh, to simply be a guest and not a working participant! Fun!

Spent $6 on admission to the Fair on Saturday, another $9 on funnel cake (with powdered sugar) and roasted corn on the cob. Friends treated us to our demolition derby tickets ($8/each).

Overspending goes hand in hand with unhealthy fair food. Refrained from buying apple butter, peach butter, cinnamon apple butter, and apricot butter. Luckily, I really only had $20 in cash, so I put a couple things on my card, and stuck to cash only the rest of the time. Total spending was about $32.50.

I wanted to treat them to lunch on Sunday for putting us up and all, but didn’t get the chance to. I did run their dishwasher for them, though. Imagine that, an Asian using the dishwasher to wash dishes! Such a novelty.

The real plan is to trade them manual labor (babysitting, cooking and cleaning) later this summer when I have time on my hands. We’ve been such close childhood friends that we’ve never practiced such etiquettely habits as host gifts and bringing wine to gatherings before, I guess there’s no reason to start formality with practically-family.

March 20, 2009

It’s funny how an increment of $10k can evolve a game plan. Now that we’re past anticipation of and well into preparation for the layoff, I’ve been dabbling with numbers and colors on Google Docs spreadsheets. I need to know we’ll be “ok” if this trend of employers passively rejecting me, ie: not calling me back, continues.

Multiple scenario budgets have been projected based on remaining unemployed through December 2009. Barring emergencies, they reveal that:

A) We will be ok until the end of this year.

B) Assuming unemployment will supplement savings, we’ll survive beyond the end of this year.

C) I can afford to take at least one major trip (<$2000). For sanity's sake, I can't afford not to take that trip.

These revelations are fairly reassuring, at least until the New Year, at which point full scale, high grade panic will commence if I don’t have a job nailed down. It doesn’t matter if I still have $30k in cash. Without cash flow, I will be freaking out. Consider yourselves warned.

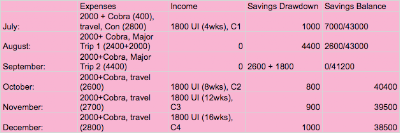

These three iterations made the most sense for modeling purposes.

Scenario 1: With full expenses, no major travel, unsubsidized Cobra

Scenario 2: With full expenses, two major trips, and unsubsidized Cobra

Scenario 2: With full expenses, two major trips, and unsubsidized Cobra

Scenario 3: With full expenses, two major trips, and subsidized Cobra

Scenario 3: With full expenses, two major trips, and subsidized Cobra

Notes

A) Both vacation and severance payouts are estimates, to be paid at the beginning of July.

B) “Travel” money every month is just an allowance. It’s not much, but you better believe I’m not just sitting on my butt at home all day every day.

Some thoughts. If anything goes wonky with severance and vacation, knock $5000 off that starting savings total. That’s a just-in-case. We’ll likely know by mid-June if they intend to be obstreperous.

I’d like to contribute $5000 to my 2008 and 2009 Roth IRAs, so subtract $10,000 total from the savings balance. But if I end this year with no new job lined up, that leaves between $23,000- 28,000 to start the new year.

Um. No. Voluntarily dipping below $25,000 cash savings is an no fly zone. Going below that number makes me fear for the still-nascent house fund, among other things. $30,000 would be much better. $40,000, even better. But you can see where this might lead: no trips, no rest, no travel, no life, no balance. While I’m fiscally conservative, timidity in financial planning is not my thing.

Speaking of fear, everyone’s fearful now so, according to Buffett, it’s time to be greedy. Not too greedy, but I do want to set aside some non-retirement investing money while the market is still trashed. Buy low, yes? A thousand bucks’ll be plenty because that low, low price might very well turn into zero.

After some consideration, I think this is the plan:

1) don’t allow anything to go awry with severance and vacation. Don’t mess with my money, boss!

2) don’t contribute to my 2009 Roth.

3) do contribute to 2008 Roth. ($-5000)

4) consolidate emergency cash into a single account, probably a money market given the state of my existing “high” yield savings accounts.

5) continue job hunting

6) plan an awesome trip that includes educational facets that I can add to my resume

7) find a few CDs and create a CD ladder for some of that money

8) research stocks, see if I can muster the confidence to commit to a few

If 2010 dawns with new job secured, I can contribute to my 2009 Roth, salt away something for the emergency fund while replenishing the expense cushion, and start seriously funding the house account. Ideally, that new job would require a move of reasonable distance and affordability.

Lists and spreadsheets laying out possible outcomes in a situation largely out of my control helps me focus my attention where it’ll do the most good. Then I can look at this job loss dead in the eye and call it opportunity.

March 17, 2009

I’ve been doing some research on all applicable benefits that I need to address, secure or continue after the layoff, most of the information I need is available at my employer’s website. I’ve truncated some of the information for clarity’s sake. It’s very important to make these decisions while I have the luxury of time to think about it because the website explicitly states:

Enroll within the deadlines. If you do not act by the deadlines, you will not be able to purchase the coverage at a later date.

Medical and Dental Plans

Coverage ends on the last day of the month in which you terminate.

* You may elect to continue your coverage for up to 18 months (COBRA). HMO participants who exhaust their initial 18 months of COBRA coverage may be eligible for an additional 18 months under Cal COBRA. Your election must be returned to the Benefits Administration office postmarked within 60 days from your termination date or the date of notification, whichever is later. If you do not elect COBRA within 60 days, the COBRA opportunity is forfeited. You will pay the full premium plus a 2% administrative fee.

~ It’d be ideal for me to schedule my last day in the first week of the month if I have a choice. (Doubt it). If I leave due to securing new employment, I should not *fingers crossed* need to worry about COBRA. I’ll keep the paperwork on hand anyway, just in case.

Something I did NOT know before: according to this New York Times article, I should try to wait until the end of the election period to take COBRA to avoid paying for those two months of coverage if possible. If it turns out I needed coverage in Month 1.5 post layoff, I can just make up the two months’ worth of premiums and still be covered. I will, of course, check with the benefits department to make sure that’s true. And get it in writing. 🙂

Life Insurance

Group coverage ends on the last day of the month in which you terminate. Coverage may be converted without evidence of insurability if you apply within 31 days of termination.

~ If I haven’t selected outside insurance by that date, then I’ll convert. For the time being, I’ll apply for supplemental insurance at 5X my current salary in case I want to take it with me. The life insurance quotes I’m getting aren’t so attractive.

Accidental Death and Dismemberment Insurance

Coverage ends on the last day of the month in which you terminate. Conversion to an individual plan must be made within 31 days of termination.

~ Do I really need this?

Long Term Care

Coverage through payroll deduction ends the last day of the month in which you terminate. You can continue coverage by making a direct payment to the insurance company. Your premium remains the same. Contact the carrier directly within 31 days of termination to convert to direct billing.

~ Continuing negotiations with my dad. Better make it snappy!

Old Retirement Plan

If you have satisfied the vesting requirement and the present actuarial value of your benefit is less than $5,000 when you terminate employment, you will need to take action regarding your benefit. If you do not take action regarding your benefit, we will cash out your money to you if the value is $1,000 or less. If the value is $1,001 to $5,000, we will rollover your money into an IRA. If the value is more than $5,000, you cannot receive payment or rollover the benefit but will receive retirement benefits based on its value when you retire.

~ Vesting was dependent on 5 years of employment so I wasn’t counting on this. It was funded entirely by my employer so I wouldn’t be out of pocket but when I got in touch with the plan supervisor, she told me I was auto-vested when they changed our plan. Nice! I will roll it over directly into my Vanguard account, but she won’t tell me how much it’s worth until I know that my time here is done.

Current Retirement Plan

Your contribution to the Retirement Plan will be taken from your final paycheck. Supplemental Retirement Plan contributions are not taken automatically. Contact your investment company or your benefits office to discuss options regarding your retirement account.

~ Simple, I have enough in the these accounts to maintain my relationship with Vanguard after separation.

Flexible Spending Accounts (FSA)

You may submit claims for eligible dependent care services incurred through the end of the calendar year in which you terminate. You will be reimbursed up to the amount remaining in your account. Expenses submitted for reimbursement must be incurred prior to your termination unless you elect COBRA continuation of your health care FSA on an after-tax basis.

~ Will make sure to be seen by all my doctors, have prescriptions filled, and costs reimbursed before we’re outta here. Doesn’t make sense that I would continue FSA on an after-tax basis since the point is that it’s a pre-tax benefit.

Tuition Assistance

If you leave during a semester, you will receive a pro-rated fee bill and are responsible for paying the cost of tuition for the remainder of the semester.

~ N/A for me. Unfortunately, I never took advantage of this benefit.

Looking back, I’ve been quite blessed to have such comprehensive benefits even if I didn’t fully maximize all of them. Other than the health care, the tuition reimbursement could have paid the largest dividends over time in terms of furthering my career if I could have made time to attend classes. On the other hand, I did manage to earn a major raise by working my butt off instead of taking classes, which was hugely critical to my ability to pay the bills, pay down debt, and save so much. If I can land another job with similar benefits, I will definitely take advantage of free (though taxed) education!

March 1, 2009

Not only is WAMU still charging the stupid $25 annual fee for 2009, they’re also charging a $75 distribution fee, costing my already depleted IRA fund a total of $100 in fees. Unbelievable. At this rate, I’ll be lucky to retain half the value of my original contributions. Then again, I only had several months to contribute at that employer after I turned 21, and before I quit, so it wasn’t a huge amount of money to begin with.

I would have balked, and did mentally, but sting though it might, this is the smarter long-term choice. Paying a hundred dollars now to roll the remaining money into my current employer’s plan under Vanguard is the equivalent of 4 years’ worth of annual fees. That money better be sitting in the retirement account for much longer than 4 more years! That’s my breakeven point.

This should have been done as soon as I established my retirement plan with the current employer, but I didn’t realize that it could be incorporated into my 403(b) without tax implications. In retrospect, it’s already cost me more than a hundred dollars in fees (a $40 distribution fee was charged when I first rolled it over). This is for keeps because I’m signed up for Vanguard’s emailing service which eliminates annual fees on my accounts and I have enough money in Vanguard to just keep it there once I leave this employer.

Just another stupid tax from back when I didn’t know to look out for fees charged for moving my money around. Come to think of it, I was shocked by the $40 distribution fee back in 2004, and could have sworn that I asked about it, but cannot for the life of me remember what the answer was. The cost of naivete and inexperience.

February 15, 2009

While arranging a baby shower, I sent out all the emails to the family invitees, but had to call the grandparents because they don’t use email. The extended family is like my adoptive family, and I’ve celebrated countless holidays and life events with them, but I’d never really just called up and chatted with them. Sent holiday, birthday and thank you cards, talked to them on the phone when they called friend’s home, yes, yes, yes, and yes, but this was a first.

You know you’ve got an entirely different generation on the phone when the second question they ask, 90 seconds into the conversation is, “where are you calling from? Home? This call is going to cost you a fortune!”

🙂

“Sorry, I misunderstood what you were asking; I’m on my cell phone and have unlimited minutes, don’t worry!”

And with that, I had a lovely 30 minute conversation with each grandma, each happily assured that they could chat with me as long as they liked without incurring long distance charges. They’re great!

The first one wondered why I was doing “so much work” for the shower, and why I was doing it. Well, I said, gosh, her momma told me to. 😉 Oh, and besides, she’s my BFF. (Haha, her mom really did, but I would have anyway. The girl’s like my sister, and her family’s always been so good to me, there’s no hesitation in making parties happen for her.) She cracks me up, she told me that Grandpa wanted someone in the family to marry me so they could keep me around. Well, the boys are like my brothers, so that’s totally out.

The second one wanted to know all about how I was doing, and we talked about the economy, the family, her kids, how she’s taking care of herself. I subtly suggested that we get her computerized to get rid of her paper files since she was having trouble finding some boxes since the holidays, but she’s a packrat. The second I asked, so you really want to do this? She backed out! Oh well, thought I’d give it a try! 🙂

Sometimes I forget how great family can be when they love and support you. And they’re hilarious too, because G2 tried to freak me out telling me that she was fine because all her investments were “with Fannie Mae, Freddie Mac and AIG. You know, all the financials.”

“…….. you’re just trying to give me a heart attack.”

“haha, no no no …. ok, yes, I am.”

December 30, 2008

It feels like I’ve been on a 12-step program for pending resignations and layoffs. Despite recession fatigue, and family nonsense, the following plan has kept me on track even while I internalized the news, and updates on a daily basis.

1. When signs point toward instability, tell no one connected to your current workplace that you’re looking unless you absolutely trust them and they’re a good resource. Commence resume polishing and editing.

2. Contact mentors and trusted colleagues for feedback on resume and verify that your previous references are still relevant and willing to serve.

3. Form a mental target: what are you looking for and why? It’s very important not to look at it as something you’re running to, in desperation, or a means of escape from something awful. It can be, there’s no doubt, just don’t let that be the motivation that fuels your search. Make it positive: make it about where you want to go next, what new challenges you’re looking for, what inspires you? This may not be concrete in your mind. It certainly wasn’t in mine three or four months ago, but it’s solidified as I’ve refined my search and dealt with the everyday challenges.

4. Speaking of everyday challenges, don’t forget to do your job to the best of your ability while you still have one! If you’re using this 12-step program, you’re still employed so you should stay that way until you are ready to move on. Give your employer no reason to target you for an early layoff and derail the plan. Paychecks are good.

5. Search relevant job boards, selecting possibilities that most closely match your new goals.

6. Refresh: take a few minutes a day, or a lot of minutes every couple of days to refresh yourself: take a walk, play with your pets, do anything that’s not work and job related. Juggling job hunting with maintaining your existing job and keeping everything together can be intense.

7. Cover letters! When you have a group of possible jobs that you’d like, write or edit your existing cover letters to address the requirements of each job. It took me about three months and several fresh starts to hit my stride. Templates are great, but only once you have a strong basic template to work from; some of those standard letters I’ve seen are weak sauce. You’re not weak sauce, don’t let your letter say otherwise!

8. Request recommendation letters. I prefer to keep hard copies with my resume in case of interview.

9. Prep your interview skills: review possible questions and answers with a friend. Mentors are wonderful people – if they’re able and willing, draw on this resource! This is great for your confidence in phone interviews which should then lead to face to face interviews.

10. Prep your interview wardrobe! I nearly had an aneurysm when I was asked to pick an interview date, and I still didn’t have a THING to wear. (I’ve outgrown the old suit.)

11. Repeat steps 4-7 until you have need of 9 and 10. Very importantly: keep on saving your pennies, nickels and dimes while working toward your next step. The healthier your emergency fund, and the safer you feel financially, the more confident you’ll be. That directly translates to better negotiations, and a more discerning job hunt. Remember, if employers can smell your fear or desperation, you’re either a less respected candidate or not a candidate at all. Either way, bad times for you!

12. Knock ’em dead!

Aside from some fretting, (or a LOT of fretting sometimes) it’s been slow but steady progress. I count my blessings where I can find them:

~ I’ve got strong recommendations

~ I’ve got great skills in my area, and a very strong work ethic

~ I’m setting up freelance work starting now to keep an income stream no matter what happens here.

~ I’ve got my readers and fellow bloggers for moral support and cheerleading – priceless!

If anyone has advice or stories to share, please feel free to do so!

December 8, 2008

As we approach year’s end, my mind is drawn irrevocably into evaluation mode and I assess how I’ve done this year and what methods worked or didn’t work for me. I like to work through this stage before the holidays so that I can create a new plan for the following year. As I grow as a pf blogger and budgeter, I’m learning and sharing what I learn as best I can.

One of the basic tenets of personal finance is that setting goals is critical to growth. The smart money says that setting Specific, Measurable, Attainable, Realistic and Timely goals is the best way to achieve your aims. I’m not sayin’ what it was, but SMART money my money wasn’t.

I’ve failed miserably at setting and achieving SMART goals this year. Psh, there was a time I quit setting goals entirely. When I admitted that, there was a moment of guilt for being so disorganized, or even unmotivated. Because that’s what it was, right? If you’re not even willing to set a goal (and let’s face it, I wasn’t trying) then clearly there’s no motivation.

You know what, though? That wasn’t true. Despite all my lofty goals from the end of 2007 that I didn’t actually accomplish, like buying a house, or investing, or saving half my salary, I still made some progress this year. No, it wasn’t Specifically what I had in mind, I had trouble Measuring it sometimes, other times it seemed downright impossible (A) or crazy (R), and nothing happened quickly or in a Timely manner. But if you look at the whole picture, it’s a different story than just a failure to achieve. (And if the markets were kinder, it might even be rosier than that. But never mind them.)

See: a year in review

Despite a few challenges……..

It’s been a tumultuous year to say the least, even discounting the whole economic meltdown, but it hasn’t been all bad.

I’m seeing that the smart way isn’t the only way, and that’s not necessarily a bad thing. All this time I didn’t understand how money can be such an emotional issue, or why people would choose the psychologically satisfying rather than mathematically efficient method of getting out of debt, or growing an income. Looks like I was wrong!

If I had insisted on following just the straight and narrow road by setting strict goals and assigning Passes or Fails, I would have felt terrible about it. It was difficult enough to K.I.T. (keep it together) well enough to focus on the big picture, and take little steps without calling myself a failure 6 out of 7 times a month.

A comparison of my finances from last year against this year shows an increase of about 20%; keeping myself on a looser leash worked out pretty well. You could rightfully point out that it’s not that significant because I didn’t start out with that much. That’s true, but I am ending the year on a relatively healthy note and that’s nothing to sneeze at. Having stuck to the basic principles of reducing expenses, increasing income where possible, and maximizing how far each dollar went, we did pretty ok this year.

Editor’s Note: Flexo posted about Taking Control of Your Finances today, and he has a few other good reasons SMART goals might not be applicable to your situation.