May 4, 2010

Revanche and Single Ma’s $5K/5K Challenge

Yesterday I announced a joint 5K challenge that Single Ma and I are taking on and we’d like you to join us!

The goal:

SHE: Single Ma starts training on May 2nd and hits the race starting lines on June 5th.

ME: I will be saving every penny not needed for expenses and aiming for the highest possible amount by June 5th.

The details: She doesn’t expect a perfect race, and I don’t expect a perfect savings run. I know that $5000 is a huge sum, and I really want to hit that goal, but to make it realistic, I’m setting some ground rules.

First: I won’t cheat by skimping on every day necessities in order to artificially win this challenge. For example, if I owe gifts to people, they won’t be sent late because I’m trying to avoid spending. On the other hand, whenever I can use gift cards to avoid using cash, you can bet I’ll be doing so.

Second: Since I do not make well over $5000 in any given month from my day job, savings money has to come from my freelance income.

Third: (The equivalent of walking) I will allow any invoices for work already performed paid during this timeframe to be counted toward the total. The converse is also true: I will not book any money that has been invoiced but not received. So if you owe me money, please pay me during this time! 😉

Fourth: Accountability! I will be posting weekly updates to my savings regimen.

FAQs

Q: “WHY WHY WHY?

A: Well, it should be obvious why SM is doing the 5K – she’s insane! 😉 Nooooo, it’s a great milestone to achieve. As for me, I have some major savings goals for the year and this is one way to concentrate on reaching at least one more early in the year. The more I bank, the better my position will be in as more family challenges crop up this year.

Q: Why match SM?

A: SM’s always been inspirational and I know many of her readers feel the same way. The symmetry was poetic and I couldn’t turn down the opportunity to “run” with her!

Q: What if I can’t save $5K?

A: Not a problem – set your savings goal wherever makes the most sense for you, but make it more than your usual savings rate. The point is to stretch yourself beyond the normal day to day.

Q: How do I have to save for it to count?

A: You can save however you can so long as you’re not lying, cheating or stealing. Small bits, lump sums, getting your cousin Sally to pay back that quarter you lent her when you were both 7 years old, if it’s ethical, it’s fair game! 🙂 Also, no neglecting your responsibilities!

Q: What if I don’t blog, can I still participate?

A: ABsolutely! If you blog, and you’re taking on the financial challenge, please do post the challenge and weekly updates. If you don’t blog and want to send your numbers to me, you are most welcome to comment and/or email me and I’ll keep a spreadsheet with our progress. This is a team effort!

May 3, 2010

In one month, Single Ma of Fabulous Financials fame is going to take the leap into her first 5K race! Having blazed the trail to financial success in her life, she’s refocused her intensity on a new frontier. If you’ve missed her fabulous (of course) tweets in the past few months, she’s been making major changes in her lifestyle, overhauling her eating habits and kicking the crud out of the Couch to 5K program.

She starts official training for the 5K today, Sunday May 2nd. Starting at the same time, I will be “running” alongside her in the saving spirit – I will aim to save $5000 between May 2nd through June 5th.

Will you join us in Financial and Physical Fitness?

Stay tuned for the details!

April 26, 2010

This is probably the most important detail in the whole process of budget-making: how do I ensure that I have saved a substantial amount by the end of the year, even on an incredibly tight budget?

Step One was establishing my bottom-line expenses. I know that they will increase but for now, I need to know the precise minimum I *must* have.

Step Two was establishing my savings wish list. This is what I want and mean to have. On a meta-level, I know that I have a priority list and can switch priorities as necessary.

*Investing in a 401(k) will be automatic and basically invisible.

Step Three was re-establishing my time commitments. I rely on alternate income to make up the difference between the regular income and the goals and that requires careful time management so that I don’t drop the ball on either side.

Step Four was setting up tracking spreadsheets for the income generated so I stay abreast of the tax implications of freelance work.

Step Five is pulling it all together: as income is earned after the month of April, a set amount will go towards the expense fund and the rest will go to savings. All alternate income goes toward the savings goals as well.

My priorities

Providing for my family

Rebuilding my portfolio of savings and investments

Making time to enjoy my new life

The numbers

Expenses: A very conservative $2,800 per month

Savings: I aim to average $400-500 per month on freelancing = $4950-5850/this year. That takes care of my debt to self which is the same as 50% of my Emergency Fund rebuild goal. I would then take the rest and stash it in the insurance and maintenance funds.

It’s a little disappointing to see the numbers are so low, but any other windfall gigs aren’t included in that total. It’s ok, this is a work in progress.

{———-Bonus Round———}

And we now know that I have to budget in extra money for further medical treatment and therapies for my mom (to be determined) as well as to move them. Look forward to Budgeting, Redux!

April 22, 2010

[This budget was developed before

Sunday and

Monday‘s situations, so of course it’ll have to change to accommodate the new developments. But I worked hard on it, so this series is going up anyway!]

These goals are beyond stretch goals since my disposable income doesn’t actually cover saving an average of $2900/month from the end of July through year-end. That’s fine, I prefer to set high goals and find ways to meet most of them than settle. Some of these are overlapping from the previous post so they’ll look familiar, or they might have been expanded. Until my benefits and paychecks settle out, which they will by the end of May, these goals will remain soft.

Long term Savings Goals

Emergency Fund: Doesn’t need too much work. I’d like to ratchet this up to $40,000 by next year so that I can roll $20,000 into any decent interest-bearing, mid-term CDs.

[Need: $5,400]

Expense Account: It’s less than half its former glory. Let’s take it back up to $10,000.

[Need: $5,000]

ROTH IRA: Haven’t made a contribution in years. Let’s fix that by April 2011.

[Need: $4,000]

Short term Spending Budgets

Taxes: If I earn enough freelance income this year, taking no exemptions throughout the year may not cover my 2010 tax liability. If that starts to look iffy, I will restart this savings account and put away 30% of all freelance invoices.

[TBD]

Auto Maintenance:

Credit card rewards alone won’t be enough to cover this category of expenses. I should have at least $1000/car per year.

[Annual Need: $2,000]

Insurance: Car insurance costs $1200/6 months for two cars. I’ll be canceling my current -very costly- private life insurance because my employer-sponsored version has become active at $9/month and “save” $41/month. Renter’s insurance is another $500/year.

[Annual Need: $2,900; current policies are paid through to October or this time next year]

Travel: Oh for an endless travel fund! Realistically, I should save for the two trips I’ve already committed to (San Diego and going home for a graduation). And maybe two more trips back home this year.

[Need: $2,000; have some travel credit on hand already]

Clothing: I must have a budget for 2011. The budget strings will simply be too tight for me to steal a little bit here and a little there from the Expense fund like I used to do (shhh!).

[Need: TBD]

April 21, 2010

New job, new salary, new savings goals

Ever since landing the job I’ve been on fire to write up a new budget and set my savings goals for the year. With a new set of demands on my income, I had no idea how much I’d be able to save but I’m bound and determined to work it out.

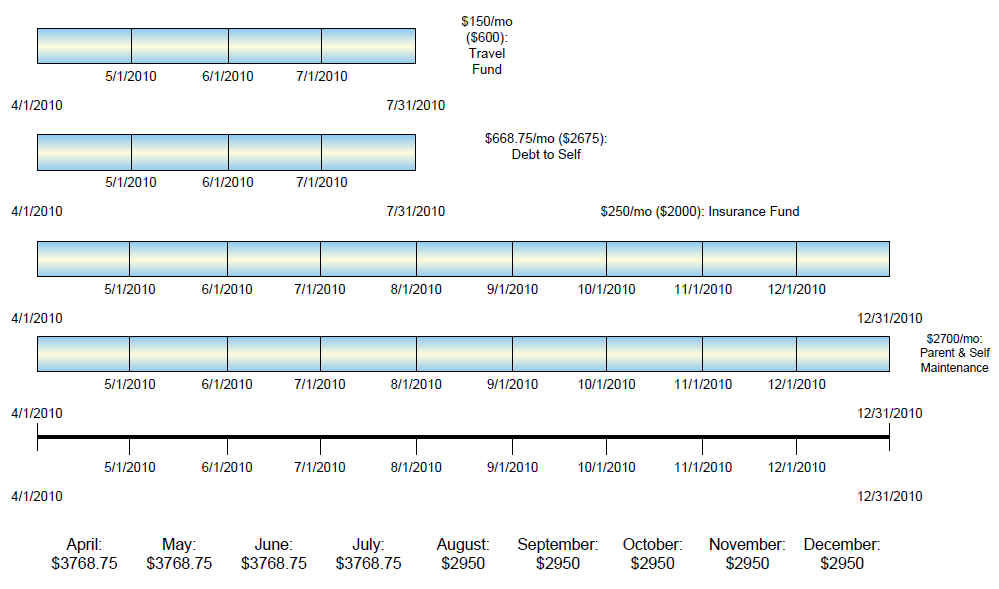

Let’s look at my major obligations

In a nutshell, the graph shows these items:

$2700/mo – allocated for all household expenses (my parents + mine) [SPEND]

$668.75/mo ($2675 total) – Debt to self to be repaid by July [SAVE]

$200/mo ($2000 total) – total amount needed to pay next 6-month auto policy and the monthly savings amount to pay annual insurances. This estimate might be a little on the high side but I need to replenish my insurance fund. [SAVE to SPEND]

$150/mo ($600 total) – travel fund minimum by July [SAVE to SPEND]

Those monthly totals are more than my salary alone can provide, so it’s good to know how much more I need to earn through freelancing. It’s stressful seeing a shortfall, but better to know than not! To be honest, none of that’s actual debt either, what I’m really planning are my short-term savings goals above.

[This budget was developed before

Sunday and

Monday‘s situations, so of course it’ll have to change to accommodate the new developments. But I worked hard on it, so this series is going up anyway!]

{————-CARNIVALS————-}

April 3, 2010

As always, every little bit counts! And as always, you’re welcome to share!

From me

Don’t leave home without your coupons: I already know this, but I still did it. Having promised myself a few additions to my rather-shabby wardrobe, I went into a Martin + Osa to poke around, certain I wouldn’t find anything. Sure enough, sale and regular priced items were equally out of my price range.

I tried a top anyway, and a sales associate attached herself to me. She kept bringing me more clothes to try on, trying to figure out what I was looking for in the “semi-business casual” sense. Normally this annoys me to no end, but she didn’t. We piled up an impressive array of clothes that didn’t fit, and a small stack of clothes that did fit. The only problem? She’d pulled clothes that weren’t even out on the sales floor and there’s no way I was going to buy without a sale AND without a coupon.

I explained that I’d left our (20% coupon) at home because I wasn’t expecting to shop, and that I’d love to buy that day but didn’t feel comfortable spending 20% more than I would have with the coupon. Was there anything in-store they had on hand?

She produced a Friends and Family coupon for the entire purchase which was actually better than mine by 5%. I ended up selecting enough to constitute a Major Purchase so I saved $65 after spending a whole lot more.

Another banking goof: During an internet blackout/packing frenzy, I missed topping up my checking account by just a few dollars. A stupid mistake was costing me $34, until I reached a Citi rep over the phone and explained that I’d been unable to get online to transfer money. The fee waiver was immediately credited to my account. Back to keeping a bigger cushion and closer eye on the checking account.

The missing link: Shopping for a belt at Kohl’s, I was again, unarmed with a coupon. At the register, I asked the cashier if there was a coupon out that I’d forgotten to clip and she said, “I’m sure there’s something out there, I’ll just give you 15% off!”

March 22, 2010

“Finite means, and deciding how to spend them, has a delicious tension that infinite means can’t supply.”

– From Carla Power’s The Pleasure of Pinching Pennies on Oprah.com

I can’t tell you know much I love that sentiment. The paragraph continues …

“If the lamp’s genie had granted Aladdin limitless wishes instead of just three, where would the fun be in that? The link between thrift and being fully engaged with life’s possibilities was recently noted by Barbra Streisand, of all people. Back before she got famous, she had to stretch her $45 clerk’s salary all week. “Those were amazing times,” she told a talk-show host, “when you have your future ahead of you, and the challenges of making that $45 last, and appreciating every penny.

Spoken like a true multimillionairess, you may scoff. The glamour of making ends meet frays pretty fast when you’re worried about losing your house or going without health benefits. There’s thrift, and then there’s fear, and nobody should confuse the two. But for those fortunate enough not to want for basics, there is a glorious discipline in trying to stretch your money to fit your vision of the world. Like a good workout, or great sex, weighing up how you spend your money recenters you, allowing you to feel the reach and heft of yourself moving through the world.”

The distinction made here between thrift and penury is critical — there was absolutely nothing fun about working 80 hours a week, trying to make decent grades in college, all the while wondering if I was going to bring home enough to pay both the rent and utility bills. There was nothing glamorous about dropping silent tears over my checkbook, willing the numbers to match up and stay in the black.

But years after that was over, when I graduated and started making a little more money, I made choices for myself. I started to appreciate what was truly important and why they meant more to me than eating out or buying Stuff. My parents’ choices made more sense: buying used clothes; handing clothes down through four cousins; only allowing me to borrow, not buy, books; and helping displaced family with comparative luxuries like take-out food, money and shelter. It took some years before I realized that they were making perfectly acceptable sacrifices for their kids to provide basic necessities to our extended family.

When you have just enough to get by, your choices are your values. Your lifestyle brings out the grit and creativity that usually hides deep in your bones.

_____________________________

My post on buying a car (should I or shun’t I?) was included in this week’s Carnival of Personal Finance! ’twas rough times out there, the Carnival is overrun by the classic ninja vs. pirates vs. nuns vs. fighting robots vs. real estate agents vs. zombies!