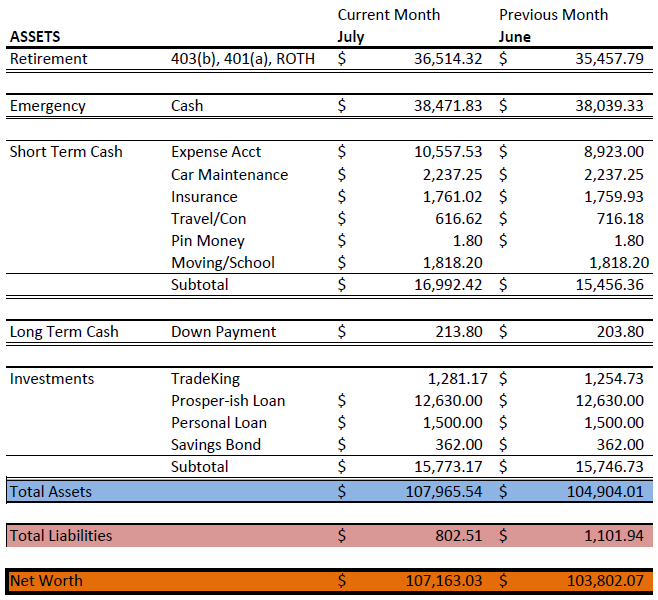

July Snapshot

August 1, 2010

Katamari Accounting: I think it’s time to roll as many accounts into one as possible.

- 1. The Retirement Funds are now spawning a 4th account due to the rollover I initiated a couple days ago. Let’s make that one Roth and one “massive” IRA.

- 2. The e-fund is spread across CDs, and savings accounts in two different banks. I’d like to have two big honkin’ CDs: One is already a $15K 5-year term CD, the other might well encompass the rest of the cash as well as the soon-to-mature Prosperish Loan.

- 3. Pin Money, Moving and School just can’t make up their minds what they really want to be so they should just become Parental Medical Funds.

Financial Planning: Once I reorganize my finances, I need to help a friend structure some investments from an inheritance. We’re talking multiples of what I have personally, but not so much more I couldn’t create a cohesive plan.

Progress: It’s been a niggling thing in the back of my head that I haven’t been paying my fair share OR saving. This month’s increase, even after I paid a great deal of credit card bills off, is both surprising and puzzling. I’ve now redirected a small chunk of the direct deposit, previously all toward the expense account, to actual savings starting this month. Which brings me to ….

Urges and Splurges: In the spirit of absolute honesty, seeing my number go up when I don’t have a specific account that looks like it’s going begging makes me want want want. But ……..

Spending: As usual, binging and purging. By which I mean, I don’t get nice new clothes, underthings, hair ties, new phone, new anything that’s not strictly necessary so that I can spend several thousand dollars on my parents. They have both woefully neglected their dental care and I had no idea how bad it was until recently. I knew my dad needed dentures soon but just found out that many of his teeth are bad and so are Mom’s. I estimate that the costs will start around $10,000 for basic care.

Freelancing: If I want any extras in my life, I’m gonna have to work for it! Time to go hunting for more work.

Reality Check: Beyond that, in less than five years, I’m sure that Mom will need more assistance than Dad can provide. Heck, in two years, she could require a full scale assisted living situation and I don’t have anything near enough saved for that. Looking above, a whole $107K looks like a really tidy start until you realize that I may soon have to spend $60K/year on assisted living for my parent(s). Then I’m nowhere near ready for the future.

I would recommend doing research with regards to your options for your parents’ long term care in a facility. Medicare should pick up some or all of the tab for assisted living (which is easily $7k a month).

A key part of this, unfortunately, is making your parents poor on paper. This is what my father had to do in order to get my mother’s care paid for. Essentially he had to cash out all his stock funds and place it an annuity, pay off his home, go down to one (paid for) car, etc. They’ll let the spouse keep a home, one car, and a small income. But not much more.

This is not something you’ll be able to finance on your own. Two parents in assisted living will take every penny you have and then some.

You may have to ask your parents to move their money into your name, etc. Seek out professional guidance while your parents can still make decisions.

Could you fund a medical savings acct (or flex account) through your job? If your parents count as your dependents, you could do so and pay some of the dental bills with pre-tax dollars.

@Anon: I’m inappropriately tickled at the suggestion that I have to make my parents poor on paper simply because .. well, that’s totally unnecessary.

You might be a new visitor, or new enough not to have seen this already but I’ll add a disclaimer from now on. My parents ARE poor. Not on paper, they are, in reality, poor. Their only income is less than $500/month and they use that to pay for some alternative medical therapies for my mom. I provide their housing, food, gas, medical, everything.

So they don’t have any money to speak of, and what I have is basically what they’ll have to draw upon for long term care.

Medicare has cut back both on medical coverage and eliminated dental coverage entirely – it’s not likely they’ll cover any assisted living.

It won’t be easy but I have to find a way to finance this on my own because I’m the only resource they have.

@FS: Now that’s an excellent idea! If dependency via the IRS is the same as dependency via the FSA, which hasn’t been the case before (FSA = must be a child) that’d be a help. They don’t always correlate but I’m going to take a peek to see if it might.

Question: If you have a job, and have $37,000 in cash, why don’t you help PiC and pay some in rent/expenses or what not?

What anonymous said, except MediCAID, not Medicare. (And I am well-aware that your parents are actually poor– that’s why there’s a safety net for them once they need assisted living.)

The trick is that you need to use your money upfront to get them into a high quality nursing home. Then Medicaid takes over the payments at a lower established rate. Nursing homes are used to this arrangement– care is very expensive and can and does bankrupt families, so they have these high upfront costs before dropping to the lower rate once Medicaid starts paying. It is priced into their business models. (This is according to my grad public finance class, so the info is about 10 years old, give or take. But nursing homes are Medicaid’s largest expense.)

If your job offers long term care insurance, that would be another solution. It may be too expensive through the private market, though I was just at a talk where they talked about how little underwriting there is in LTC insurance compared to life insurance.

Here’s a link to info from the government:

http://www.medicare.gov/nursing/Payment.asp

I believe that Medi-Cal is the Medicaid for California. It’s too bad they stopped the dental services. Here’s a link to people you can contact for information:

http://www.dhcs.ca.gov/services/medi-cal/Pages/WhereToGetHelp.aspx

There are also senior advocacy groups that may be able to better help.

Medi-Cal DOES pick up nursing home costs for poor folks once they’ve spent their assets down and Medicare has stopped its payments (something like 20 days worth). It is unlikely that this particular benefit will be going away because although politicians can deal with no teeth, they cannot handle the political consequences of having our elderly dying on the beaches.

Here’s an ezine article… cannot vouch for the accuracy of it:

http://ezinearticles.com/?How-to-Qualify-For-Medi-Cal-to-Help-Pay-For-Nursing-Home-Costs&id=4508831

@Anon: Two part answer. A) The $37K is our emergency fund. My cash, but we know it’s there for both of us in case we lose our jobs or get sick, not as cash flow. B) Our agreement is that the cash flow from my job covers all my parents’s expenses, PiC & my shared expenses and a little savings towards shared goals and more emergency funding. He handles the rent but also gets more freedom with the rest of his income.

@Nicole: My dad does work with an advocacy charity group but Mom’s not old enough to qualify for other aid/advocacy groups – I’ve called dozens of groups and agencies and they have a hard age limit.

That said, research continues! Thanks for the links and the thoughts.

If your mom isn’t old enough for state aid and hasn’t been formally diagnosed with any sort of dementia, you may be able to get affordable Long Term Care insurance on the private market for her. If you haven’t looked into it (and your company doesn’t provide it as an option), it might be worth checking out.

Congrats on the net worth increase! I’m so glad you and PiC have things worked out the way you do…you have too much on your plate and I’m happy you have some day-to-day support now. Good luck on the dental bills…my husband has dental insurance and we still had to lay out $2600 for the work he’s having…