May 6, 2008

Income:

1. Ebates: $17, due end of the quarter

2. Office Reimbursements: $376, grrr…..due a month ago

3. Pay Per Post: $38, due 30 days from post

Reductions:

1. In the next chapter of Mom’s declining health, she’s consented to be removed from the car insurance because she can’t drive anymore.

Accomplished:

1. Got our local waste company to confirm that they stopped billing me for an extra barrel on 3/31.

2. I’ve got the truck posted on Craigslist *finally.* Way to wait for the recession to really kick in before putting it up for sale. *eyeroll*

Left to do:

1. My car charger‘s still not arrived yet, so I need to follow up with the company.

2. Follow up with City billing to make sure they haven’t been billing me for an extra waste barrel since 3/31.

April 28, 2008

So Best Friend suggested last night, as I nattered on about savings bonds and other financial minutiae. Heh. Yeah ….. uh … about that. No, I didn’t tell her, but I almost started giggling which would have been a bit suspicious. I’m preserving my anonymity as long as I can. I don’t want to have a debate about ending my blog because I have to be even more careful about censoring myself.

Ironically enough, a friend accused me of not being able to keep a secret last week. I’m not the source of the leak, but I almost wanted to defend myself by pointing out that I’d kept my pf blog, to which I post nearly everyday, a secret for nearly two years, and if that’s not keeping a secret, I don’t know what is.

April 25, 2008

I certainly didn’t see that coming. Sitting in my old spot by the window, but not with my back to it, exposed me to the unexpectedly worst aspect of this space: acute senioritis.

O Summer!

April 3, 2008

The secretary handed me a subscriber copy of Lucky magazine yesterday.

Addressed to me.

At work.

??

It appears, according to the mailing label, that I have a subscription through the end of the year. If my puzzlement isn’t entirely evident, I’m confused. I have no idea where this subscription came from, nor do I know why it’s going to my work address. I never send any sort of postal mail to work, that’s weird.

I asked my coworkers if any of them were trying to hint that I need help with either shopping or style, but they all denied responsibility. There doesn’t seem to be any indication that this is a gift subscription, either.

Interesting.

December 28, 2007

It’s almost sort of funny now, but a few days ago, I wasn’t nearly so amused by the conversation I had with BoyDucky’s mother. She’d been almost forcefully cheerful and friendly to me all day – highly unusual, in fact, has NEVER happened before – but I assumed it had nothing to do with me. Apparently, she was just setting me up to get me to ride with her and BoyDucky to their business, so she could give me a piece of her mind. So we could have “a discussion,” I mean.

The highlights were as follows:

1. You two need to make a decision about marriage. NOW.

2. You can’t keep living in two separate cities. Unless you’re not getting married, then it doesn’t matter.

** I couldn’t help myself, I clapped my hands and said, “Oh that’s an option? Great! We’re set then!” As you can imagine, I got a LOOK from BD.**

3. You need to find a job in Northern CA, regardless of how well you’re doing at the current job because one of you is going to have to make sacrifices. *ahem* SOME people actually quit their jobs, have kids, and then come back to their jobs years later.

4. You need to stop “chasing the money” (that’s what it’s called when you’re working instead of popping out the babies) and put your family first. (ie: yes, the family I don’t have yet because I’ve already got my hands full!)

** I was still just laughing at this point, saying “sure, one of us can stay at home. BoyDucky! He’d LIKE to stay home with the kids. I’ll work really hard, get some major raises and be the breadwinner.” That screwed up her tirade for a few minutes. She regrouped, though. What a trooper! **

5. You should just quit your job here and, if you can’t find a job like you’re doing now, just go be someone’s secretary. You’d probably be good at that.

** Laughter stopped. **

6. What are your parents doing? I think your dad should just get some job somewhere and work for someone. Or maybe he just won’t lower himself like that. What’s your mom doing? etc. etc. etc.

** The funny left the building. **

I keep hearing that I shouldn’t have high expectations for a MIL, that some MsIL NEVER become reconciled to the DIL until they’re practically on their deathbeds (in one case, literally) but is it really so unusual for a MIL to have a little respect?

Leaving aside the whole can of “how dare you judge my parents when you know nothing about them” worms; I doubt that anyone who had any respect for me would suggest that I dump everything I’ve labored so hard to accomplish to go have babies on their say so. Not because it’s a priority for me, but because she wants grandkids and the other kids aren’t giving it up. Is this a generational thing? The one that dictated the older generation would give everything up to have kids and take care of them? I highly respect my parents for the sacrifices they made, and return the favor in kind, but giving up everything for kids I don’t have (and maybe, don’t want) yet is not happenin’.

Besides, it’s just not practical. I already have two dependents, and taking away my income to live on BD’s doesn’t work at all.

Is this as laughable to anyone else as it was to me? Or does it just sound familiar?

Ok, I guess it’s not that funny now that I think about it. Just kind of sad. But boy, she got me good with that secretary thing. After all, it was just a probably that I’d be good at it! All kinds of implied insult. *eyeroll*

November 26, 2007

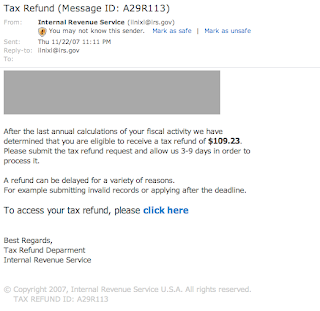

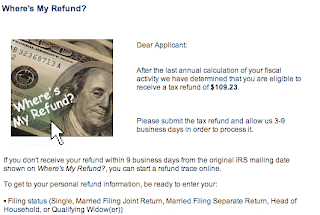

On Thanksgiving, the scammers thought they’d give me a bit of holiday cheer by sending this cute little message:

And because I’m a mean girlfriend, I immediately checked the IRS website to confirm that it was a scam (which it is), then called BoyDucky over to take a look at the email without telling him what it was. I knew that he’d think it was kosher simply because I didn’t say it wasn’t. But he’s got to learn more skepticism! It’s my mission to foster suspicion and paranoia in my compatriots so that I don’t have to worry about them. And you. Don’t fall for the IRS scam, folks, it’s not worth the $109 they claim you’re owed.

And because I’m a mean girlfriend, I immediately checked the IRS website to confirm that it was a scam (which it is), then called BoyDucky over to take a look at the email without telling him what it was. I knew that he’d think it was kosher simply because I didn’t say it wasn’t. But he’s got to learn more skepticism! It’s my mission to foster suspicion and paranoia in my compatriots so that I don’t have to worry about them. And you. Don’t fall for the IRS scam, folks, it’s not worth the $109 they claim you’re owed.

Oh, by the way, if you do click on the link, it looks pretty good until you realize they used Comic Sans on the image. That’s just not IRS-style, scammers, they use HELVETICA.

I reported the link, and now the site is tagged with a warning that it’s probably a fraudulent site. That’s pretty cool.

November 18, 2007

Confrontations: My brother took the car, seeking permission from my enabling father instead of me, on Thursday. I’ve had it out with both my parents for their enabling behavior and finally got a hold of my brother today to give him a piece of my mind for his selfish, thoughtless behavior. I’m taking away his car keys this time, like I should have last time. I’ve also taken away my parent’s keys. How has my family life come to this??

Discoveries: I can probably bid on a one or two year subscription to the Wall Street Journal on ebay and NOT spend $100 on it. The seller requires at least a 30 day history on ebay and have positive feedback due to “non-payers.” I have no recollection of using ebay to purchase anything, but because I had ordered books on half.com 6 years ago, that history translates to ebay! Turns out I have a 6 year history on ebay and 100% positive feedback. NICE. That’s useful IF I win this auction. In the meantime, the website has a pop-up offering me a two-week free online subscription.

Also, I found a stock-conversations friend. Never had one of those before. It’s all very new, but it was good motivation to finally bite the bullet and start investing a little. It’s not that I’ve done all I can with regards to the “less technical” (as I see it) personal finance, it’s just time to expand my horizons. My eyes did start crossing a bit when the conversation got more technical than I’m accustomed to: dividends, divestitures, equity …. oy! My understanding of how stocks work is still shaky. Time to do some research.

Delivery: My ETS check came in the mail on Saturday! +$98! Will have to put that into the Expense account, though. Projected expenses through the end of the year are higher than I’d originally expected.

Acquisition: All the doomsday predictions about Comic Con selling out their 4-day passes even earlier this year got to me. I bought my pass.

Difficulty: BoyDucky’s father took yet another turn for the worse this weekend.