June 3, 2009

Remember how happy I was when I finally rolled over my Rollover IRA?

The pure joy may perhaps be less than obvious, but it was there, I promise. About three weeks after that happy occasion, I received Another Statement from my former brokerage. Wha?

Two cents. A dividend of two cents paid out into the account that was safely and finally closed, keeping it open. Then Chase, in their ongoing brand conversion, opened up a brokerage account for me funded by those two cents. I could just imagine trying to do something with that two cents and being charged another annual service fee. AUGH.

Grumpiness and inertia kept me from doing a darn thing about it until I received a Welcome to Our Brokerage Services! letter yesterday, complete with account number and phone number.

A few minutes later, a friendly fellow with Chase Brokerage services ran a solution by me: write off the two cents and close the account. Yes!! Thank you. They can have that two cents if it means one less account for me to deal with.

March 13, 2009

And here’s what’s been rattling around upstairs:

1) Want to save more. How can I save more? (Assuredly, this period of binge-saving will be followed by a period of purge-spending. Just came off that spell a couple days ago.)

Thanks to the recent spate of car activity, monthly expenses have come down by $500. That‘s why the expense fund seems so robust. That can be directed to savings right away. What else can I cut out?

2) If the period of unemployment lasts through, say, the end of the year, I’ll have missed out a lot on retirement contributions. The goal is to have a lot of cash in the cushion, but what if some of that cash were stashed? Not too much of it, but an uptick in contributions seems like a good idea. It’s the opposite of DCA – investing in large lumpy sums for the next three months in anticipation of none at all from July through December, but I think it’s better than nothing at all.

3) Speaking of stashing, what about diversification? Ought I revisit the trad/Roth IRAs? There’s still time for 08 and 09 contributions.

During this period of uncertainty, cash certainly reigns (and yes, I still want my 50K of savings for lack of a more secure position) but there’s always an itch to earn more than sub-2% interest rates.

Grocery store scores:

Last night’s trot ’round to the Fresh ‘n’ Easy turned up a 4-pack of “snacking apples,” 4 for $0.75 marked down from $2.89. They were a bit over a pound, so that’s not a bad per pound price.

Also, the red russets were 3 lbs for $2.88. On the pricier side until checkout revealed a $1.88 price tag.

Certainly not a comprehensive shop, but it was a quickie run, primarily for a fruit for lunch tomorrow. Meant to grab a couple of the monster-sized burritos at $2 per, they looked to be at least 1.5 pounds but I couldn’t be sure they would last the weekend for next week’s meals and I’m not sure that I wanted them for the weekend. All told, never came near to using the $2 off coupon. (Minimum purchase, $10).

November 25, 2008

Been having myself a little pity party over being sick since I went to bed early but kept waking up and feeling worse each time I did. I’m not a morning person, and that not wanting to get up increases exponentially when I’m sick, because that’s always the worst part of my days. This time, though, it’s been surprisingly easy to forget that I actually might survive until noon if I manage to stay awake and semi-productive until then – normally I just automagically find myself getting up and going to work without wasting the energy to whine about it. I guess my immune system’s a little weaker than usual.

I’ve been dazedly clicking on links from The Digerati Life trying to maintain visual tracking/consciousness, and oddly enough, the focus on layoffs and the amazingly good attitudes of recently laid-off bloggers has started to penetrate my fugue and fogginess. Amateur Asset Allocator lost his job at the end of October, so I checked on the most recent post to see how he’s been doing since. Today, he’s reminding us to roll over our old IRAs (more applicable to him since he’s no longer with his former employer) and not leave it sitting around because we’re simply too busy, lazy or some combination thereof. Very timely reminder because I still haven’t rolled over my original Rollover IRA from WAMU and it’s now costing even more ($25 annual fee) than it did before ($15).

I did, however, fight off the inertia long enough this past weekend to call United and find out that I have a nearly $300 credit in my name from a previously cancelled business trip. Heh, if the organizers were rude enough to cancel the trip without even telling me until the last minute, I’m keeping that credit! Ok, I say that like I’m rebelling, and not because the tickets were non-refundable and non-transferable. I don’t actually have a choice, it’s mine anyway. But still. It can still feel like one little act of defiance, anything to boost the spirit.

Perhaps that rolling stone of will pass the ertia along to settling the IRA issue this weekend. After all, it’s managed to lose 4 years’ worth of gains in a month, it’s not doing me any good anyway.

November 11, 2008

My online “high interest” savings accounts are anything but by now, and it’s past time to do something about it.

The odd thing is that I remembered seeing a 4.0% APY offer at Citi a couple days ago, and it’s still there when you use the navigational rate selector to check rates based on term length, or amount deposited. In other places, though, like the advert box or when you actually click through to apply, it’s 3.5% APY. What gives?

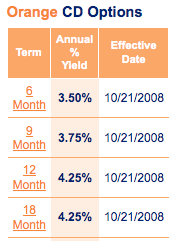

I should roll over some of my emergency money (it’s spread across three different accounts because I didn’t want to be stuck without any e-money if one of the banks were to encounter problems) in the Citi and ING Direct accounts to CDs since they’re short term and I don’t anticipate needing all of that money upfront. (Oh great, way to tempt fate, self!) Looks like both of them offer a 6-month 3.5% APY right now, so I don’t even have to feel torn between one or the other product.

Then again, I could create a CD ladder with ING:

The only question is, is that really feasible considering CDs are just a bit less than liquid vehicles? I’m crap at math sometimes, bear with me. If my e-fund is at 6 months’ worth of expenses, and I don’t need to touch it for another two months (approximately), I would be safe putting up to 2 months’ worth in a 6-month CD. If I were to need access to the money starting in two months, I would need four months’ of cash (12,000) before the remaining money (8,000) was available at maturation.

That puts paid to the idea of creating a ladder with this money for now. Oh well, just a thought.

June 26, 2008

Boston Gal’s posting of this WSJ article about folks who are cutting back on their retirement savings made me feel guilty.

I know that I had a perfectly good reason for doing it, but it still stings that not only did I cut down, massively, on contributions, my account keeps dropping like a rock and doesn’t even reflect the amount of contributions I’ve been making since the beginning of the year. At this rate, I’ll never crack $25,000! [I’m not talking about overall, just between the 401(a) and 403(b).]

Ok, that’s not guilt I’m feeling, I’m just disheartened.

The important things to remember:

1. The reduction is temporary. It does not affect my match because I’m maxing out the 401(a) which is the only account that is matched.

2. Finances have to be flexible to accommodate when life happens. Obstacles are inevitable, and stubbornly stashing hefty amounts in my retirement fund while cash flow suffers does not make sense.

3. I’m simultaneously working on reducing all expenses so as to narrow the gap between expenses and income. This reinforces the temporariness of this solution. I’d like to see the gap closed in a matter of months, but it’ll take some more mathing, when I have time.

April 30, 2008

If I’d read this post yesterday, and known to fill out Form PD F 5374 yesterday, I could have sent PaDucky to the bank to purchase paper bonds for me. Instead, I banked on getting my Access card in the mail by today, which I miraculously did, and proceeded to input my password incorrectly at the website, and lock myself out of my brand new account.

Argh!

No savings bonds with a decent interest rate for Ms. Miniducky. Boo.

Called Treasury Direct and left them a message in a futile gesture, hoping that thye really would call me back tonight and that the recording “Please leave your information, the customer service representatives are all busy now but they will call you back.” wasn’t just a cruel cruel tease. Yay.

It wasn’t. Yay.

I missed the call. Boo.

I called back, and they actually picked up! Yay.

I managed to reset the account. Yay.

I started my transaction, and the confirmation page said, “We may have moved your purchase date to the following business day.

May 1, 2008.” Boo!

So, in the end, still nada.

And just to rub a little NaCL in that wound, it turns out you can only convert paper bonds when they send you an invitation to do so!

Boooo!

April 29, 2008

In a singularly daft move, I sent off my signature authorization form off to Treasury Direct without my SSN. In trying not to advertise my SSN while obtaining the authorization, I forgot to write it in after I returned to my desk, and just blithely sent it off. A nice lady at TD called me two days later to let me know, and I didn’t even question it. I just called back and gave her my SSN.

Now, it’s unlikely that someone would know that I was signing up for an account, know my cell phone number, and time the call so it’d sound entirely plausible that I’d forgotten such a detail, all to steal my SSN, but there’s a very paranoid part of me that thinks, You fool!!

I didn’t even check the TD website for a general contact number to verify that there was indeed a Nice Lady working there who was processing my paperwork.

The nice lady followed up with an email to my private account letting me know that the hold was removed and to expect an Access card soon, though, so I’m probably ok. Really, stupidity does come in threes.

*Note: Rats. I should expect the Access card in ten business days. 🙁 I wonder if I can get to a bank during business hours today or tomorrow ….*