February 17, 2009

1. Positively antsy to get my/family taxes completed. Yes, this is my confession that I did not offficially file my taxes myself, again, this year. Gah. I’ll feel guilty about it later. I did my usual dry-run, and I think I’ve finally gotten things straight. If they match the accountant’s, I’m filing my own next year. *goal set!*

2. Got two ING Direct referral bonuses in the last week, courtesy of Flexo‘s awesome link-sharing policy. Thanks Flexo! [If anyone wants one directly from me, I’d be happy to send you one!]

3. Still waiting to see my check for the truck insurance refund. How sad, just $115. Stinks that they refunded it to a card I canceled, so I have to wait for that card to send me the check.

4. Expect to be doing the same run-around with the insurance refund on the sedan.

5. Food makes everything better: we’re going to potluck next week. This should be good.

January 29, 2009

Kelly at Almost Frugal posed the question: How much extra are you willing to spend?

In this case, she’s looking for a new bed for her daughter. Her mother suggested that she just consider how much EXTRA she’s willing to spend over a baseline price for the item. The theory behind this is that she’s going to pay the baseline price anyway, the only consideration is how much a premium she’s willing to pay on top of that.

That’s very interesting: I’ve always taken total price into consideration, and didn’t actively separate the purchase price from the premium.

In coming weeks, this purchasing perspective will be very applicable to my personal shopping needs. If a new apartment is in the works (I hope I hope!), I’m going to need some basic furniture and tools. Mostly kitchen stuff, and a basic tool kit.

Major factors include distance (how far will I lug stuff) and space (do I have room for stuff). The most significant issue, of course, is cost. Since I don’t anticipate any crazy signing bonus, not a normal thing in my industry anyway, what I’ve got in the moving account is what I got. (A whopping $1498, if you’re curious.)

It’s a balancing act: take enough stuff – avoid shelling out cash for new stuff, pay to haul stuff.

Take too much stuff – no room for it, costs money to lug it to destination.

Take too little stuff – minimize moving expenses and buy at the other end.

With that in mind, I’m debating what to keep and what to leave behind.

A few months ago, my assumption was that when I moved, my parents would be moved out into a smaller, cheaper apartment. Reduce cost and required upkeep: less stress all around. Turns out, around here? No such thing as a cheaper apartment.

Get this: we’re paying as much for our rent (3 bdrm, 2 bath house) as some folks pay for a 2 bdrm apartment. Can you believe that!? We have the amenities of a single family home (in home laundry, no share-the-wall neighbors) with the associated utility costs. Most importantly, though, we have the freedom to keep our pets. My sole surviving dog of our former 3-pack is a large breed, and no apartment within 30 miles will allow her breed or size. Not even for a premium. And there is NO WAY I will turn out my dog. None, nada, nope, never.

After parking, laundry, fees, and pets are considered, it doesn’t look like we’d be saving more than a few hundred per month, if that. That means that staying put is an option, and that means that I could keep some of my heavier (really old) stuff in my room. Renting out one room to help with cost is a possibility, but I could also still keep my room and have a home base.

The desk: is a 12 year old heavy particle board executive desk. (Yes, I was a spoiled brat and *needed* the 6 foot wide desk with a hutch. We paid way too much for it. But I’ve used every inch of it and work at it every single night.) Doubtful that I would take it with, it’s survived a couple moves but it’s way too heavy for me to haul up and down stairs. I’d like to be as minimalist as possible in case I have to move all by myself.

The bed: is a 13 year old twin day bed. Same old frame and mattress. I’d like to take it with because it can be set pretty high off the ground to create extra storage space vertically. For once in my life I’d love a double, but it’s not a need.

The bookshelf: it’s comin’ with me! I use a deconstructible (uh, is that a word? I’m not a wordsmith today) steel framed bookshelf. Nothing fancy. Just four shelves in black, and I like being able to hook things into the zigzags of the shelves.

A storage bench: this comes with me too. I got this storage bench from Ikea, unfortunately in white, but it’s great because it’s got foam padding on top and storage inside. A decent bed in a pinch. Maybe I’ll just use that as a bed until I get a good deal on a real one?

Chair: I don’t even know how old this desk chair is, but the hydraulics still work, it’s got enough padding on the back to serve. It’ll go with.

Lamps: My friend gave me his extra floor lamp a couple years ago and it’s still working well, as is the ten dollar Target desk lamp that sits by my bed. Both go with.

Misc (Clothes, shoes, and books): I think the books will be the heaviest since I have so many paperbacks and trade paperbacks (comics). They’re my indulgence! I have pared down the paperbacks, pulled out about 150 of them and a good friend who shares a PaperBackSwap account with me listed them for swap. It’s awesome, I supply the books, he supplies the labor, we share the benefits of getting cheap books.

Some basic clothes will stay here, but all the comfy and professional clothes go with me. I’ve already spent a lot of time paring down here too, but I could use another concentrated go at it.

Same with the shoes: some will stay here, but I’d like to make sure we’re down to the essentials only. The definition of essentials will depend on where I go.

Kitchen: there’s nothing in this kitchen I would take from my parents, other than a few favorite glasses/mugs. Maybe the Brita. My parents don’t like it anyway. For that, I’ve got about $80 left on a Bed, Bath and Beyond gift card and some coupons. A pot, a pan, a few dishes and utensils from Ikea should do the trick.

I wonder if it’s too early to set my baseline prices for a bed and desk substitute?

I’m not sure if I’d be willing to yard sale a bed, but a desk would be fine. Perhaps I can hold out on shopping until yard sale season?

January 25, 2009

And no, I’m not crazy, Dish Network retention services department guy. My time is worth more than …. nothing!

Finally called Dish today, for what seems like the 875th time in the last year and a half. Their website keeps sending Yodlee bills for a total of $46.37 at last check, while never actually allowing me to view any bills or statements. This annoys the heck outta me because I should be getting free service for at least another 8 months! The previous 870 calls were about actual statements I was receiving in the mail for services I kept trying to cancel; this is a new twist in their game.

It turns out that the amount is a credit on the account to offset the automatic billing of $10.81/month, but I’m fed up with my budget tracking getting screwed up by the errant billing every month. And we don’t use it anyway, so I asked Nick to, please, just cancel the account.

“You …. want to cancel your free cable?”

“Yes, I know it sounds crazy, but please please cancel it. I’ve spent WAY too much time on the phone with your CSRs, not that they weren’t perfectly nice, but waaay too much phone time has been wasted over this account.”

“Um, ok, if you’re sure….”

So that’s it. A box should be sent out, a neck will be risked to remove the thingy from the roof, and they’ll stop telling Yodlee I owe them money. I hope.

November 14, 2008

It seems that the average consumers interviewed for this NY Times article, Lower Gas Prices Don’t Make Americans Feel Rich, aren’t taking the relief at the pump for granted. With the increasingly bad economy, and fearful outlook for the future, it relieves me that people aren’t simply reacting to the lowered prices with the same exuberance as we’ve seen in the volatile stock market.

I’m glad. It’s time we were more cautious, paid down debt, and made plans for a rainy tomorrow because I’m afraid that many people are already headed for a rough time of it without such back-ups. Even with all my preparations, saving, and thinking ahead, I don’t feel quite as prepared for a downturn of the proportions that are likely to come. No, the sky isn’t falling, but some days it feels like the ceiling might start caving in, and the floorboards have a decidedly creaky feel to them.

Speaking of temporary reprieves, we just got news of a reorganization in our office, effective Monday. The manner in which this decision was made and the suddenness with which it came to pass took everyone aback, and I’m not convinced that they’re not planning to reorganize us right out the door. Might not happen Tuesday, Wednesday or Thursday of next week, but it could happen the day after. Or the week after. Nothing’s certain but at least I have an e-fund. And I haven’t tempted Murphy, thank goodness. Either way, it’s not exactly the Christmas present I was hoping for from Santa!

November 11, 2008

My online “high interest” savings accounts are anything but by now, and it’s past time to do something about it.

The odd thing is that I remembered seeing a 4.0% APY offer at Citi a couple days ago, and it’s still there when you use the navigational rate selector to check rates based on term length, or amount deposited. In other places, though, like the advert box or when you actually click through to apply, it’s 3.5% APY. What gives?

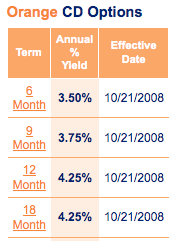

I should roll over some of my emergency money (it’s spread across three different accounts because I didn’t want to be stuck without any e-money if one of the banks were to encounter problems) in the Citi and ING Direct accounts to CDs since they’re short term and I don’t anticipate needing all of that money upfront. (Oh great, way to tempt fate, self!) Looks like both of them offer a 6-month 3.5% APY right now, so I don’t even have to feel torn between one or the other product.

Then again, I could create a CD ladder with ING:

The only question is, is that really feasible considering CDs are just a bit less than liquid vehicles? I’m crap at math sometimes, bear with me. If my e-fund is at 6 months’ worth of expenses, and I don’t need to touch it for another two months (approximately), I would be safe putting up to 2 months’ worth in a 6-month CD. If I were to need access to the money starting in two months, I would need four months’ of cash (12,000) before the remaining money (8,000) was available at maturation.

That puts paid to the idea of creating a ladder with this money for now. Oh well, just a thought.

October 28, 2008

About two weeks ago, I saved an acquaintance from getting a ticket. The metered spots only allow 4 hours of parking before a certain time in the evening, and she’d run out of meter time an hour before Free Time. As parking enforcement rolled up, glancing over at her car, I popped out and dropped some money in her meter.

When I drove into work last week, I used the meters because I normally commute by train and don’t have a long-term permit. Absentmindedly noted that I needed to move my car at 4:50 after parking …. then, I completely forgot until 5:50 pm. I was in agonies, sure I’d been ticketed.

Whether it be because I’d earned a little non-tickety-karma by helping someone else out or because there was construction on the street, there was no ticket on my windshield. Hallelujah for avoiding stupid-absentminded fees!

October 3, 2008

The long-awaited quarterly check has arrived and I am positively stoked.

I am so close to having six months of living expenses in the Emergency Fund!! As soon as I have at least $1000 in the mini E-fund, my plan is to [finally] close the real E-fund to all non-critical withdrawals.

All the bills for September have been paid and I still have $1300 in the Expenses fund. With the deposit from the quarterly, I have enough for October’s expenses on October 2nd. All paychecks earned in October will continue to add an allotted amount to the Exp. Fund, but I won’t be waiting on them to pay the bills. Holy cow, I could pay the entire month’s bills on October 1st. I won’t, of course, that’s not the point of the cushion. The point is that I could if I needed to. Whew!

So I discovered a few things wrong with my math. The quarterly is for the past three months of work [July 1st-Sept 30th], so plotting the total expenses against income through the end of December means I come up short, ie: depleting most of the expense fund by year’s end.

What I need to do is fund the supplemental portion ahead of the next three months. In other words, instead of taking July-Sept money, and only setting aside three months’ worth of income to make up shortfalls from July-Sept, I should set aside enough for July through December. Then, I’ll be covered and still have the cushion in place through the end of December. Then the last quarterly check of the year [Sept through Dec] funds the various accounts that I’d previously planned for this check: Savings, Insurance, Car Maintenance, Travel, Moving, etc. That means I’ll be funding it for 2009, at the end of 2008! This makes much more sense.

All OT can now go towards other sub-expense funds instead of just savings and expenses. I expect an insurance bill in November and I don’t quite have enough for that yet, so OT will fund savings and insurance for the next month and a half.

Also, I’d goofed on the October paychecks, so I have to rewrite the plans for 4 paychecks in the next two months, not three. And actually, now that I’ve fixed the above problem, that third paycheck can come at any time, it’s no big deal.

It’s very strange budgeting on a hybrid [half regular-half supplementary] income. The supplemental is scheduled and the amount is set, so it shouldn’t be difficult, but I haven’t done it so very well since this started. Might I now be starting to get the hang of it?

Perhaps I’ll even get my September snapshot in order now that I’ve reconfigured the economic landscape …