January 17, 2014

Yep, I said it. I’m still Happy New Year-ing y’all. It’s been busy!

This is how I know recovery is nearly complete from the Devil Flu + infectious friends: my brain starts insisting on money talk. This is the first chance I’ve had to really look over last year’s money and do a quick review. We combined our finances last year and started to work from a combined budget spending plan. That was rocky, we have totally different perspectives and styles when it comes to money. Still, we had to start somewhere! So we did.

2013 highlights

SPENDING

We went over (between 2-100%) the budgeted amounts in half our specified categories, and under (between 2-50%) in the other half. This was, of course, a disappointment. Overall, we overspent 20% over and above the budget. Most of that, as it shakes out, was the wedding but that was paid for in cash so that’s some solace. I’m NOT thinking about the travel we could have paid for instead. 😉

I do have to keep reminding myself that we pay about $17,000 annually for my dad’s upkeep and that makes a big dent in the disposable income.

SAVING

We maxed out PiC’s 401(k) contributions which has never been done before. WOOT! We also saved 25% off the top of our paychecks through the whole year. Two thumbs up!

Disappointments: I don’t have a retirement plan through the new company so I intended to set up my own. Researched, yes. Decisioned, no. So that’s a fail.

BEST OF

The renewed relationships that came out of planning the wedding. I mended fences with a few relatives that I haven’t spoken to in years. And even more surprisingly, for whatever reason, MIL suddenly thawed towards me a month before and spoke to me like she hasn’t since before PiC and I started dating. Whatever the reason, however long it lasts, I’m grateful that even if I’m not “part of the family,” we can actually behave like non-antagonistic humans. That’s all I ever wanted.

Also: savings. We actually did a good job of saving cash despite all the spending 🙂

Also: Year of the least number of bad surprises (like the car was towed because they didn’t tell me that they were behind on payments! or like, Mom fell and hurt herself! or, Mom was in the hospital with pneumonia for a few days!)

WORST OF

The pained and strained relationships. It’s like I’m just now living the teenage angst years that I never had with my parents, with my dad. Nothing he said when it came to the wedding planning was ok, it was always inflammatory to my overly-sensitive, culture-betraying mind and we argued A LOT. Unnecessarily, I think but it was hard to rein in those feelings. 2 days before the wedding that I had a long painful talk with him over how his reactions made me acutely aware of how I’d failed the family: how I’d failed to straighten out my brother, how I’d failed to provide for my mother, and how I was now failing to properly represent the family as a “dutiful bride”. In turn, he reminded me that I’d done the best I could and more than was expected, and a big portion of these ‘failures’ were his; that the fact that he couldn’t “give” me a wedding was a huge failure as a parent. That he was making his peace with my decisions and in the end, he only truly cares about whether PiC and I are happy. I really needed to hear that. I just wish it hadn’t taken several months of fighting to get there.

Also: no retirement plan for me. This is the first time since age 21 that I haven’t been investing in retirement. No bueno!

:: What were your bests/worsts? How’d you do with saving/spending?

November 20, 2011

I’m back. Thank you for all the thoughts and condolences, everyone.

It’s a -something- getting my head and feet back where they need to be so, as usual, I turn to working with finances for comfort.

We’re nearly through November, so at this point, I don’t know what to call this.

Retirement Accounts

Just as I predicted, my new retirement account through my “new” job (I guess I should call it the Now Job) is fairly mediocre to poor.

Overall Rate of return on the new 403(b): -4.94%

Balance over 1 year timeline: 747.01 to 6661.87

All the increase is in contributions with losses, not gains.

Vanguard rallied this month, though.

Brokerage account

This account sees steady (tiny) increases every quarter generally. $700 of that 1,915.05 is just cash I’m holding for a future purchase that I may or may not make. Still, neither of my stocks have lost money over the time that I’ve held them (though it only matters at the time I sell) and one pays dividends so it’s throwing off income in the meantime. A whole $4 every quarter!

Cash

There was a modest false bump in the cash calculations because I locked myself out of my Ally Bank account at the end of September and never bothered to get back in again. That’s where my CDs are and so I haven’t been getting accurate data on the interest earnings for the CDs.

It turns out that my cash holdings passed the $50K mark this month after recouping the cost of the funeral from funeral gift monies and adding the remainder (a very modest amount) as a separate category to take care of remaining costs as they come.

Spending has been OUT OF CONTROL though. In the week we were down south, we spent more on gas, food, and incidentals than we’d normally spend in a month, I think. I haven’t had time to comb through everything yet.

New

Family Budget:

I’m creating a combined budget for our money going forward. It’s sort of good timing in that we’re at the end of 2011 anyway, so I’m taking all our liquid cash and pooling it to create a fresh set of household funds similar to my current set-up.

I’ve never had this much to work with but there are two of us in our little family and Doggle now, and two extended families to plan ahead for. Now I need to figure out which banks to use.

Mortgage:

We’ve explored some refi options and I am now pondering on the wisdom of the financial risk we’d be taking in committing to one or another of these options. More research to come!

Benefits:

Now that we’re married, we can combine our benefits. Costs will go up on PiC’s side, and go down on mine. I don’t think we actually come out ahead, though, as I do the math.

Insurance:

It’s time to reevaluate the cost of our auto, home and other insurance. We currently carry our insurances separately, of course, so it’s time to see about combining them for cost-effectiveness and discounts.

Upcoming Spending:

* We need a new mattress for the bedframe that PiC Craiglisted earlier this month. I really hate mattress shopping. All those options and I can’t tell the difference in how one mattress feels from the next, but there’s this imperative to pick the right one because you’re going to have it for a trillion years. And you know the bargain hunter in me would absolutely have to know we’re getting the best deal possible. It’s possible I’m a little more gripey than usual about it because I’m tired but … I’m probably exactly as gripey as I normally would be.

* I need to plan our Christmas shopping – I already have some small gifts for other people earlier this year but there are primary gifts for family that haven’t been bought yet.

In sum: Tons to do and I feel like I need to do it all right now. Surprisingly.

October 5, 2011

I don’t even have the heart to post it, the progress has been so meager in the past two months.

Retirement Downturn

Since the last time I viewed my Vanguard fund, the fund that contains all the retirement monies I’ve saved between ages 21 through 26, it’s lost another $7000. In two months. !!! Yes yes, long term horizon, blah de blah. STOP THAT.

I’m still contributing to my current employer’s retirement account but that’s in a different fund at a different company. It still irritates me. I’ll stop looking now.

Cash Savings

The expense account did come up a significant amount (40%) but so did my spending (220% over last month). That figure’s actually misleading though – $1200 of that cash is a reimbursement for business expenses and so are the corresponding credit card charges. Part of it is prepayment of expenses as well.

Also, we are experiencing the first true combinations of expenses between PiC and me. We have combined forces to rack up all chargeable expenses on a single American Express card to meet a minimum spend threshold in order to earn a 20K point bonus for Starwood points.

On that plan, I’ve prepaid 2 months’ worth of cell phone bills, paid up on auto insurance and vet bills. O, vet bills.

Other Investing

I had grabbed a chunk of cash for my TradeKing account in case I made a decision about investing in a few more stocks. I’m steadily making a whopping $4.70 every quarter in dividends from my stocks. With the huge dive in the market, I thought there might be a worthwhile discount to buy. Nothing really caught my fancy, though, so that cash is still just sitting in the brokerage, waiting.

Total Net Worth

Up about a thousand dollars. I should really be doing better.

******

Specific Spending:

Wedding/Honeymoon: The reason we’re racking up the hotel points and miles is to defray upcoming travel spending. As much as possible, I’d rather use awards to pay for actual travel as much as we can. Starwood points are excellent for hotels and for exchanging to airline miles as well. They add a bonus 5,000 miles for every 20,000 miles you trade in.

Mortgage: I’m keeping an eye out for any other good refinancing options that we could qualify for and considering how quickly we might pay down the mortgage.

Saving Goals:

Emergency Cash: I’m really close to the $50K cash cushion that I wanted to hit for my peace of mind. It’s in a combination of CDs and savings accounts but I need to find a higher rate of return home for it. Or ladder all of it into CDs.

Then I think I’m setting my next cash savings goal at another $50K. The first $50K is total emergency fund only. (Hey, remember when you could earn real interest on CDs and such?)

Pie in the Sky? As an academic exercise, I sort of want to map out how we might work out life on a single income around here. Just to see what that might look like. Or perhaps one and a half at first.

Non-notables:

I don’t think I like spinach anymore.

Doggle now gets time outed. And he knows when he’s misbehaving so when he’s getting walked to time out, he walks himself the rest of the way.

August 7, 2011

It’s been a while since I’ve posted one of these. Over six months, in fact. I have been keeping track of some months but it’s been sporadic. Life has been consuming.

In the past six months I’ve ….

– been traveling which still hasn’t been fully documented.

– loving my Doggle (talk about for better or for worse!)

– started, stopped, got sick of planning, budgeted for (on paper), and started saving for a wedding that I still haven’t actually started planning again.

– consolidated all of our phones onto a cheaper cell plan to save money.

– gone to My Mecca (SDCC) with bloggy friend.

– generally worked on surviving the master plan of earning my way up the ladder. I need a new plan, this one is beyond exhausting and doesn’t leave any time for real life.

There was far more spending than saving in the daily scheme of things but in the background, the automated investing and savings allocations are ticking along, doing their jobs. I had a glance over my Vanguard funds’ performance the past four months to find that they’ve horrifically lost all their gains of this year:

Huge losses. Just huge. Given the turmoil in the government this month, I can’t say August’s losses were a surprise but it’s an eye-opener.

And except for that last item (working my tuchus off) which, though it paid off, has me pondering those workaholism tendencies, infiltrating all corners of my life again, it’s not necessarily the worst way to have spent many months. More rest, though, would be wonderful, and I want (nay, need) to see far more progress in the savings ledger in upcoming months.

With the state of the economy, the uncertainty of the jobs market, the recent downgrade of the credit rating, it’s time to do massively better.

This isn’t just prompted by general concern for the state of the union or personal insecurity, though. I’ve done that “what happens in case of a layoff” exercise a thousand times. And I’ve done it in real time. This isn’t that faux-planning; this stems from wanting to grow beyond the rat race.

When I start making choices in the near future, I want real choices, not just be limited to picking from the limited array that my employer at the time is offering. Which means that if we want One Frugal Girl’s flexibility if we decide to start a family and get thrown a curveball in the process, or if we want to consider adoption, or we want to move out of the Bay Area, we definitely need financial security in multiple forms.

Besides, working into an early grave isn’t precisely the endgoal, and staying in this routine, driven by my need to achieve in the confines of a traditional environment, is setting myself up for that very thing.

January 8, 2011

Overall, a fairly solid increase from last year, I’d say, across the board through another rather turbulent year.

During 2010…

My mom’s health… huge turn for the worse. The downward spiral continues. I still can’t accept the disintegration of my family unit as I knew it and still struggle with the fact that this idiot won’t grow up. But PiC managed to save the year.

I combated the depressing months of job-hunting and fruitless interviews with massive decluttering efforts. Then I landed a job and had to move. Enter all sorts of soul-wracking guilt and abandonment remorse. And more shockingly, a measure of peace and the slow drain of rage from my life. It turns out moving was good for me. So is cohabitation. Which was also a surprise.

Cooking and cleaning became a more regular and pleasant part of life, and as predicted, work kicked my butt for months. I was miserable, regretted it, detested it, and ultimately said, there is no way you’re going to beat me. Eventually, I prevailed over the worst of the problems, and the rest are just part of the job.

I’ve been quiet here for lack of energy and brainspace but that’s slowly coming back.

There’s been travel, there’s been life, there’s been love. There’s finally a sense of potential again, and to be perfectly honest, that scares the skivvies offa me.

Looking forward…

There’s a lot of work still to be done. My parents need moving, but my dad’s become much more proactive in working on these things I’ve been talking about for years. While I still don’t necessarily agree with some of his decisions about my mom as they’re born of stress, short-sighted, and made in a “spare the daughter and spare her money” mode, he’s trying his best and I can push them to do what needs doing when it comes to their health. Their dental repairs are nearly complete now. Only two more months of treatment to go. Thank goodness the pain is gone and the worst of the uncomfortable treatments are over.

My dearest dog is slowly fading. She’s not got a lot of time left and my dad doesn’t really like the idea of my taking her away with me since he can take care of her pretty easily as she whiles her hours away in the sun or lounging nearby. He’s probably right, but my heart aches at the thought of not being with her. I guess I always thought I could keep her happy and healthy with me by force of will.

We might adopt a dog eventually but not a puppy. We can’t be there for a puppy like we once were as kids.

[But they are so cute. For the record.]

It’s going to be a really busy year in quite a few respects.

January 1, 2011

Having skipped November, but knowing how much was spent, roughly, and how much has still gone unreimbursed, I was expecting some devastation on the NW front. It’s not great but it’s not terrible either.

Of course when I started crunching the numbers, my mind was definitely in a different place. Now it’s in a morass of logistics that haven’t even begun to start touching on budget yet so that’ll be a different post.

I’m a little bit glad that we haven’t combined finances yet. Apparently I failed to communicate with words to PiC my feelings about not needing or wanting a diamond. I just formed my opinion so long ago that it seemed like surely I would have mentioned it to him by now. I just never thought any engagement ring residing on my finger should ever cost more than a hundred dollars, at best. (I’m pretty sure that number was more generous but the closer I got to writing this, the less money I think is reasonable for a bauble …. it’s gorgeous and he spent all kinds of time picking out what he wanted for me and I don’t want to be an ingrate but .. I don’t think an engagement ring is necessary! Not for me.) That said, it’s gorgeous and I can’t really, erm, return it to put his money back in savings or anything!

Yeah that sounds terrible.

I’m sorry, it’s hard to wrap my head around the idea he spent real money on this ring. I love him and I love why he did it and he knew it was entirely unnecessary, just taking me some time to reconcile.

Also, he was snickering when I mentioned doing my snapshot because the month of November was terrible for my finances and now I know why. *faint* At least he didn’t go in debt.

Investing: Slow and steady, it’s finally adding up a bit.

Savings: I’m increasing the cash savings by 3% to compensate for the payroll tax holiday. I’ll have to add another fund type, clearly.

Spending: It’s possible we might have to adjust our grand travel plans after all, I’m not sure about spending $2000-3000 on a big ole trip now that we have a big unknown on the horizon. Maybe not canceling but adjustments may be necessary.

That’s all my brain has room for right now. Ta!

October 31, 2010

Back on the horse!

Contrary to last month’s assertion that I was going to just move forward and not look back, I took some time to fill in all the blanks of the past weeks’ spending and income. It didn’t take more than an hour or so and helped PiC and I have a good conversation about getting to grips with our spending as a household.

That was long overdue and makes me feel one heck of a lot better about now having a plan. We’ve got a spending spreadsheet so we’re both updating to see the same picture together and will be targeting a $400 monthly food budget. [Yes, we eat too much. We’re cooking at home a lot more but we are piggies and one of us treats other people far too much. Ahem.]

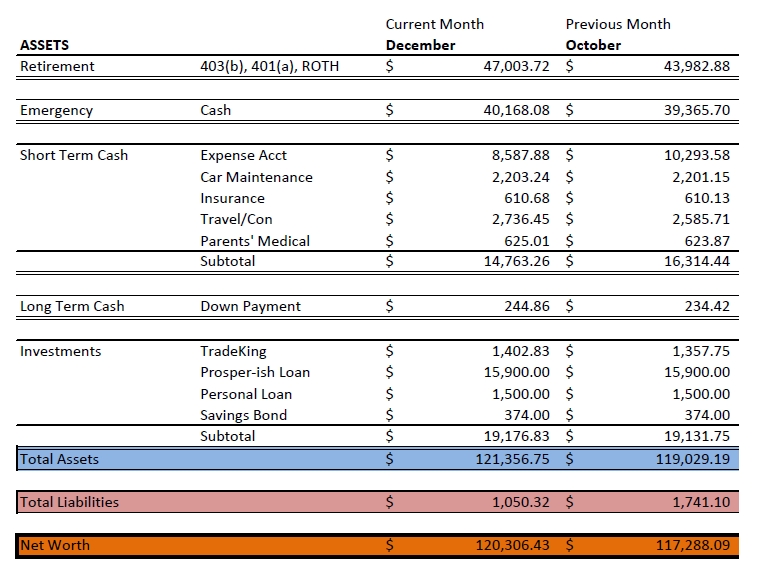

One of my private loans came up this month, hence the leap from $12,630 to $15,900. I’m looking to reinvest again so that means I’ll keep the bit over $3000 and throw the $12,630 back into the investing pool. It takes nearly five years to come due so it’s what I’d consider a mid-term investment.

I also banked that surprise bonus and snowflaked all my bits of freelancey income towards the travel fund. It’s a little selfish since the other practical funds need attention but they will always be supplemented by the expense fund if necessary. The travel fund doesn’t get that luxury – it’s either funded or I don’t travel.

November’s rent is already covered because of a really stupid mistake. The October rent was already paid at the end of September but because it came out in the month of September, my brain didn’t click and I jumped mid-October to the conclusion that I hadn’t paid so I cut another check. Everyone roll your eyes with me. Who pays rent twice in a month?? Still, let’s take it as a good sign that it didn’t break the bank.

Speaking of banks, I moved a big chunk of money to Smarty Pig just in time for them to drop the interest rate to 1.75%, which is still higher than the 1.1% at ING. Excellent timing, self.

Overall, since I’m still occasionally sneezing about my parents’ financial situation via my financial situation, I’m still on the prowl for better places to store my money for higher interest rates (hah) and more income-producing opportunities.

{kind=link}