October 3, 2010

This entire month has been so busy as to be unreal, so it stands to reason that I’m having trouble believing the net worth is real.

Every single weekend was booked: hosting friends, driving back to LA, traveling to Oregon, hosting half a dozen houseguests for days. Every weekday was booked: I started an intensive pain care program, had a birthday, and worked every weekday.

The numbers aren’t fudged, but I have felt a poor steward of my money for not quite knowing where every penny is or has gone. The last notation on my cashflow Excel sheet is September 15th, for heaven’s sake; it doesn’t make sense that it’s gone up without close shepherding. In any case, a fraction was thanks to automated savings and contributions, the rest is due to the vagaries of the market and interest payments. Next month, the phrase “keeping bills as low as possible” will be an honest factor in that. We’ve been feeding about ten extra mouths this month, I’d just be lying.

To kill that feeling of unsteadiness, I paid all my bills a few days ago, took a deep breath and I’m doing some therapeutic cleaning today to clear my head and make a fresh start. Let’s take on October!

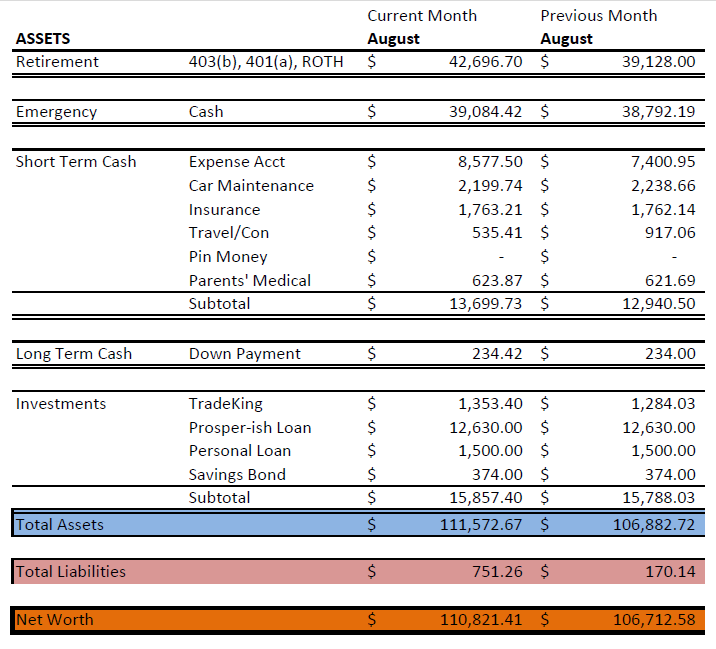

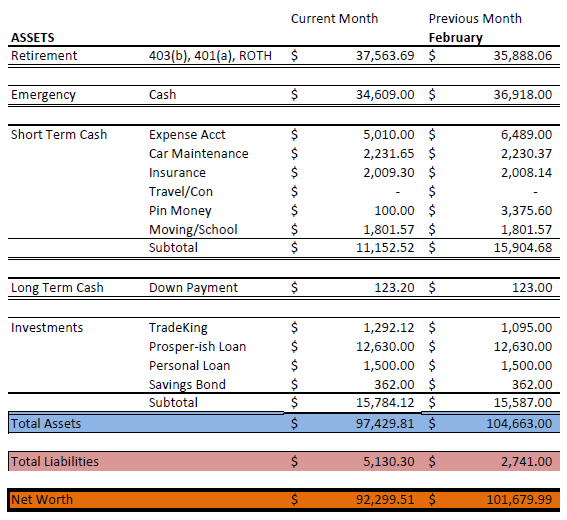

August 31, 2010

I definitely waited for the last paycheck of the month before putting this month’s snapshot together because I’ve already paid up September’s rent and paid down a 4-digit bill for the start of the Dental Bills (deep breath).

The expense account took a hit for quite a number of reasons and as we gear up for the fall, I’ve got a ton going on, so it’s only going to get worse. The medical bills are going to almost immediately drain the rest of the Parental Medical Fund so the balance will have to come out of the Expense fund. Remember, I use that to pay all bills and try to keep a few months’ worth in there at any given time so I’m not living paycheck to paycheck. I still worry quite easily when that number drops drastically, though.

A really old pension account finally rolled over into my Vanguard account, that huge uptick in retirement accounts has nothing to do with gains in the market.

I’m going to be traveling for a three day weekend in September, and I’ve got a ton of guests in town another weekend of the same month. PiC will be traveling yet another weekend, and then I’ve got to prep for a business trip in October. Before you know it, November and December are lined up right behind that with their thumbs out for a lift of multiple birthdays and holidays. Whoo! This is why planning is so very important.

As for generating extra income, I’ve been rather dismal at that. Any number of excuses really, but regardless, the end result is feeling (quite) a bit pinched after Hometown Expenses are paid, to the tune of 70-80% of my income. This most certainly needs to change!

I have been talking about second jobs (part-time or freelance) but I always get the evil eye from PiC who thinks I already work too hard. That may be, but I’ve still got bills to pay, and savings to pile up! Truthfully, there has to be a way to generate more income without unduly stressing my own health. I ought to have learned that lesson by now.

In the meantime, I’m reverting to an old method of keeping calm: noting everything financial in a notebook. That’ll help me keep track of reimbursements and other “hidden” money moving around in my system.

How goes the month for you, friends?

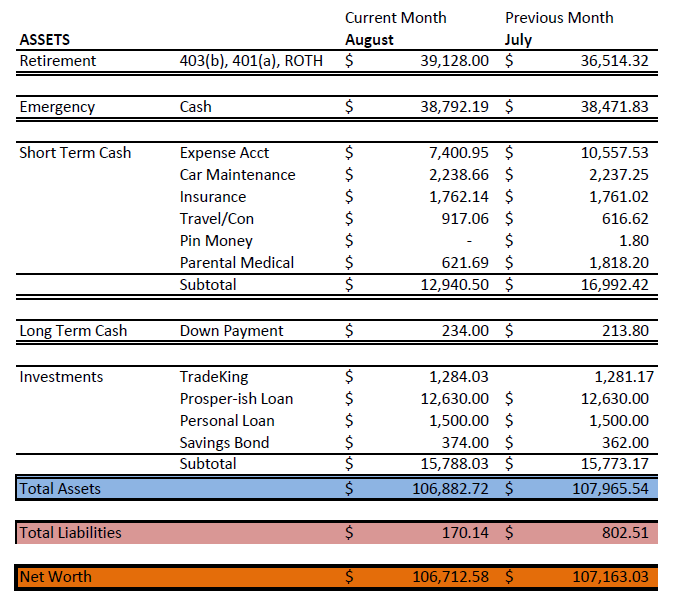

August 1, 2010

Katamari Accounting: I think it’s time to roll as many accounts into one as possible.

- 1. The Retirement Funds are now spawning a 4th account due to the rollover I initiated a couple days ago. Let’s make that one Roth and one “massive” IRA.

- 2. The e-fund is spread across CDs, and savings accounts in two different banks. I’d like to have two big honkin’ CDs: One is already a $15K 5-year term CD, the other might well encompass the rest of the cash as well as the soon-to-mature Prosperish Loan.

- 3. Pin Money, Moving and School just can’t make up their minds what they really want to be so they should just become Parental Medical Funds.

Financial Planning: Once I reorganize my finances, I need to help a friend structure some investments from an inheritance. We’re talking multiples of what I have personally, but not so much more I couldn’t create a cohesive plan.

Progress: It’s been a niggling thing in the back of my head that I haven’t been paying my fair share OR saving. This month’s increase, even after I paid a great deal of credit card bills off, is both surprising and puzzling. I’ve now redirected a small chunk of the direct deposit, previously all toward the expense account, to actual savings starting this month. Which brings me to ….

Urges and Splurges: In the spirit of absolute honesty, seeing my number go up when I don’t have a specific account that looks like it’s going begging makes me want want want. But ……..

Spending: As usual, binging and purging. By which I mean, I don’t get nice new clothes, underthings, hair ties, new phone, new anything that’s not strictly necessary so that I can spend several thousand dollars on my parents. They have both woefully neglected their dental care and I had no idea how bad it was until recently. I knew my dad needed dentures soon but just found out that many of his teeth are bad and so are Mom’s. I estimate that the costs will start around $10,000 for basic care.

Freelancing: If I want any extras in my life, I’m gonna have to work for it! Time to go hunting for more work.

Reality Check: Beyond that, in less than five years, I’m sure that Mom will need more assistance than Dad can provide. Heck, in two years, she could require a full scale assisted living situation and I don’t have anything near enough saved for that. Looking above, a whole $107K looks like a really tidy start until you realize that I may soon have to spend $60K/year on assisted living for my parent(s). Then I’m nowhere near ready for the future.

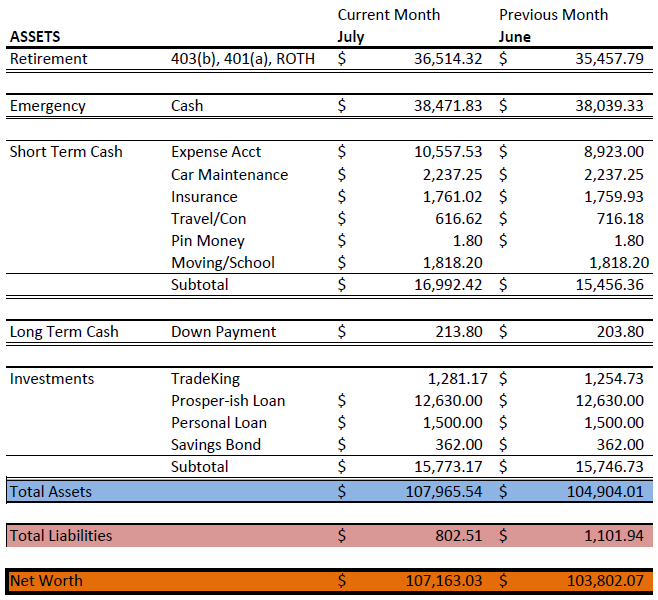

July 11, 2010

With a few minor deviations, like having paid rent for July already, I’ve pulled together what should pretty accurately reflect my financial month of June. I keep wondering if I should continue to post these reports. They were always meant to keep me accountable and make it really easy to keep track of whether or not I’m making progress, but there’s the niggling thought that perhaps it comes off as bragging after you reach a certain point.

The seemingly “steady” creep up is just the aftereffects of the great push, also known as: $5K/5K challenge. Not a penny was from regular earnings, almost every cent of that is being spent on regular expenses.

There’s something that I’ll soon, in the spirit of full financial disclosure, share with you in a future post that has radically affected my finances recently.

In the meantime, however, there are things that have to change about the picture you see above.

One, there haven’t been any contributions in my retirement accounts since I started this job. That’s because, dear friends, I’ve been a slacker in the last two months and couldn’t decide what to do about that blasted 401(k) issue. I hate passing on free money vs. I’m not convinced the match (total of 4% to my 5%, I misread the literature before) is worth the extra fees.

Two, I’ve been paying all my parents’ expenses since leaving, but I keep wondering if there’s a way I can squeeze out a little more to give them a small cash allowance as well. Although they have my credit cards, I know there’s something disheartening about never having real money on hand. That may not be possible though, because point three is…

I’d like to have at least $1,000 saved just for their dental expenses. The moving fund is in ok shape, not enough for deposits, a move, and all that yet, but I also need another $1,000 for their dental. Their coverage is, frankly, crap.

I was going to keep going but this is going to turn into a wish list if I do. Best to stick with these for now.

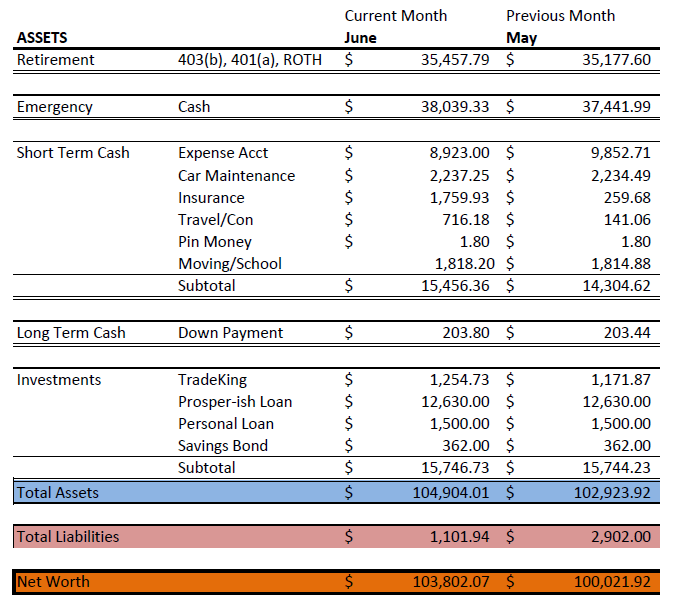

April 30, 2010

This month was an amazing turnaround from last month’s bleed-out, and honestly come by, I swear!

I’ve been working my tail off, and it paid off. The positive cashflow was nearly equal parts reimbursements, delayed invoices and missing unemployment checks showing up, freelance income, and day job income.

Cashflow in the month of April opened like a nasty joke with a negative balance of 7668.50, and closed with only a negative balance of less than $600.

I can’t really expect such dramatic progress month to month from here on out, of course, but I have to breathe a small sigh of relief that I’ve made up a lot of ground since the car. I now only owe $1730 on that debt. Soon as that’s out of the way, I can make up ground on all the other savings targets set up for the rest of this year. Exciting!

Now, I’m just happy it’s Friday, it’s payday and I can get some *rest*. Purely thrilled!

April 1, 2010

Time to face the music …..

Most notably, I’ve dropped out of the six-figure club in a big way.

1. The car: $8250. I don’t count it in the asset column because it’s a depreciating possession. True, I could actually sell it for more than I bought it for (verified by the fact that another car buying friend’s market research) but I don’t intend to turn around and sell it and have to buy yet another vehicle. I have the cash, but for the sake of full disclosure, I’m including the upcoming insurance in this total because I pay for the full term in advance.

2. Moving expenses: around $2000. Again, I included all the currently due and upcoming charges on my credit card now. No creating a false sense of security for me, thank you. Never mind that they’re reimbursable, until the money is in my account it doesn’t count.

3. I have multiple outstanding invoices for around $1500. Again, I don’t count those as cash in pocket until it’s actually in my pocket.

I’ve made a few changes in my accounts

Since the Tax account was cleaned out for the car, I’ve changed it to Pin Money for now. Essentially, miscellaneous.

Moving Money might permanently change to School Money, but we’ll see if I can get any financial aid when I restart classes again. I’m taking a quarter off to concentrate on work. That money might be donated to insurance and maintenance.

I’ve been ignoring losses and gains in the TradeKing account but there’s no good reason to – after all, I track the gains and losses in the retirement accounts.

Cash flow looks like blood flow

My transaction log shows that I’ve spent about $11,000 this month against an income of $2,700. No debt (except to myself) was created so that was all saved money rushing out the door. Painful.

Finally ….

I could really use a paycheck by the time I’ve paid off the credit cards. They don’t come due this month, I’ve just got them tallied in because the charges are posted to the account; the cushion will hold a little longer. By the time charges are due, I’ll have a couple checks under my belt. And then we’ll see how the new dual-household/single income budget works. (“DHSI” as the new acronymic moniker? Not cute at all.)

March 2, 2010

February was a tumultuous financial month, and I’m surprised that there was still some minimal progress made in the net worth growth. If anything I

semi-hinted at yesterday pans out, March will be equally tempestuous with lots of outflow and scurrying to create income to cover it. Which means: blog fodder!

Until then, my vow of Don’t Jinx Yourself pretty much means I’m keeping mum on a lot of fronts.

Taxes are filed — our accountant rose to the occasion and saved me from having to deal with my family’s financial complications. I always mean well but tax time is that time of the year I writhe in agony over dissecting my financial life, entangled with my family’s, and how that means I have to untangle their finances. It’s the one time I let my emotions get the better of me and ostrich myself with regards to money matters.

[By “rose to the occasion” I mean the family accountant called my dad with some tax suggestions before I asked the questions, and won himself my business for another year. I’m filing Head of Household again so that buys me a couple extra thousand in standard deductions and exemptions.]

Between the much reduced income stream, unemployment income (taxes were withheld), HOH filing and having prepaid a lot more in taxes than necessary, my federal effective tax rate is 10.7% and I’m expecting a rather large refund of nearly $1500. Combined with the less-large state refund, I’m going to have a nice lump sum in the Taxes nest egg. That’ll become my Car nest egg. I’ve whined on Twitter about hating shopping for a used car, and the next worse thing to that is having to finance a car.

Of course the PF wisdom is to always avoid a refund but at the end of 2008, I was more concerned about having to pay taxes (which is why I saved cash for it) and paying penalties to boot (hence the extra withholding). It wasn’t worth adjusting partway through the year once we found out that I wasn’t going to be employed post Q3 2009.

This month could have been a lot worse.